Markets struggled to find a decisive direction for the week as a whole. The dollar strengthened over the first half of the week, capitalising on the stronger than expected payroll data the previous Friday. The US currency was unable to sustain the gains and dipped weaker following the Federal Reserve meeting as rate expectations were scaled back again. The dollar did not test lows seen the previous week.

The US consumer-related economic data was weaker than expected with a headline retail sales decline of 0.1% for July after a revised 0.8% increase the previous month while underlying sales fell by 0.6%.

Initial jobless claims also edged higher to 558,000 in the latest week from 554,000 previously, although there was a decline in the number of continuing claims. The data overall will raise some doubts over consumer spending levels and triggered caution over underlying trends.

The US trade deficit rose to US$27bn for June from US$26.0bn as oil imports rose, but an underlying improvement in the non-oil account provided some degree of underlying US currency support.

There was the sharpest rise in non-farm productivity for six years during the second quarter as companies aggressively cut costs. The downward pressure on labour costs increased speculation that the Fed would be able to justify very low interest rates. Consumer prices were unchanged in July to give 2.1% annual decline.

As expected, the Federal Reserve left interest rates on hold in a 0.00 – 0.25% range at the latest FOMC meeting. The amount of agency bond buying was left on hold while the Fed announced that the US$300bn Treasury bond buying programme would be completed at the end of October rather than September as planned previously with a slower rate of purchases over the next two months.

The Fed remained cautiously optimistic that economic conditions were improving as activity was levelling out, but there was further unease over the investment outlook. The statement also commented that interest rates would stay at very low levels for an extended period with markets scaling back expectations of higher interest rates.

The Euro-zone data offered some support with an improvement in the sentix investor confidence index to -17 for August from -31.3 the previous month. There was also a narrowing of internal yield spreads which helped underpin confidence.

The French and German GDP data was also stronger than expected both registering 0.3% quarterly increases compared with expectations of further declines. The Euro-zone data as a whole was also stronger than expected with the quarterly decline held to 0.1% which helped underpin sentiment towards the regional economy.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 80% accurate. 800-732-5407

If you would rather have the recent forecasts sent to you, please go here.

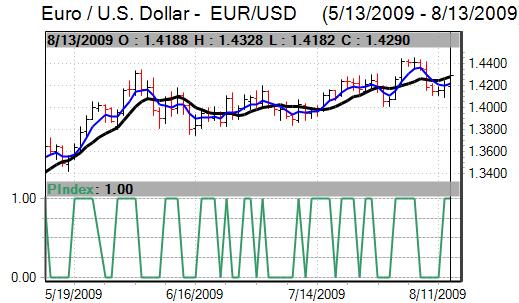

The Euro was generally weaker against the dollar over the first half of the week, but proved to be resilient and optimism over the economy helped trigger a firmer trend over the second half and consolidated close to 1.4280. The Euro was able to secure modest net gains on the crosses.

The yen resisted further selling pressure following the sharp losses seen following the US employment data. From lows beyond 97.50, the Japanese currency strengthened to highs near 95.0 and also resisted further selling pressure on the crosses. The yen gained some support when Chinese equity markets fell sharply.

The commodity-related currencies also gained ground over the middle of the week, but were unable to sustain the best levels even though risk appetite was generally firmer.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 80% accurate. 800-732-5407

If you would rather have the recent forecasts sent to you, please go here.

The UK unemployment claimant count increase was slightly lower than expected at 24,900 for July after a revised 21,500 increase the previous month, but the ILO unemployment rate was higher than expected with a rise to a 13-year high of 7.8% from 7.6% and the currency impact was broadly neutral.

The visible trade deficit widened to GBP8.5bn for June from GBP8.3bn as the oil account returned to deficit, but the gains in imports helped maintain optimism that there was an economic recovery.

Former Bank of England MPC member Wadhwani warned that the economy could face very serious challenges over the second half of 2010

In its quarterly inflation report, the Bank of England warned that inflation would significantly undershoot the 2.0% target in two years time if interest rates are increased in the first quarter of 2010 while the recession was deeper than expected. The bank was slightly more optimistic over economic prospects, although the underlying tone was still for extreme caution and uncertainty over the outlook.

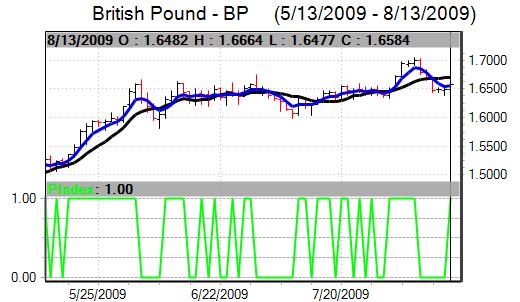

Weaker confidence in the UK economy pushed Sterling to lows below 1.64 against the US dollar. Much of the adjustment had already been seen ahead of the Bank of England quarterly inflation release which limited any further selling pressure and it rallied back to above 1.65. Sterling weakened to beyond 0.86 against the Euro.