Technical trading tended to dominate for much of the week with markets unable to break relatively narrow ranges as option-related defence dominated. Risk appetite also gradually faded during the week which provided some degree of US currency support. The dollar gained some protection as there was a gradually more cautious attitude towards risk with a 1.4800 – 1.5000 range dominating. As sentiment deteriorated, the Euro was near the weaker end of the range on Friday.

The US housing data was again weaker than expected as starts for October declined to an annual rate of 0.53mn from 0.59mn the previous month while building permits dipped to 0.55mn from 0.58mn and this was the lowest rate since May. The NAHB unchanged at 17 for October following a small downward revision for September.

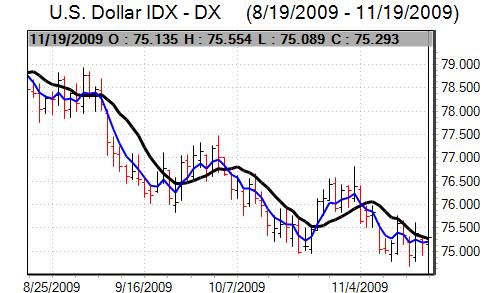

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are nearly 80% accurate*. 800-732-5407

If you would rather have the recent forecasts sent to you, please go here.

The industrial production data was also disappointing with the October increase held at 0.1% compared with expectations of a 0.4% monthly increase. The industrial and housing data will increase fears that the economy will find it very difficult to secure a sustained recovery.

The Philadelphia Fed index was stronger than expected with a further increase in the headline index to 16.7 from 11.5 the previous month. The employment component remained negative, but was at the highest level for over 12 months.

Elsewhere, jobless claims were unchanged at 505,000 in the latest week which continues to suggest a slow improvement in the labour market even though job creation remains very weak. The net impact of the data was some slight reassurance with risk appetite looking to stabilise.

As far as inflation is concerned, there was a 0.3% increase in consumer prices for October while core prices rose 0.2% for the month. Headline prices fell 0.2% over the year, but this was much less than the 1.3% decline seen the previous month and the low point for inflation has clearly passed which will complicate the Fed’s task.

Regional Fed Governor Bullard stated on Wednesday that based on previous economic cycles it was possible that the Fed will not start raising interest rates until 2012, although he also warned over the risk of leaving interest rates for too low for too long given the risk of asset-price bubbles developing. Bullard is an FOMC voting member during 2010 and the comments reinforced market expectations that short-term interest rates will remain at very low levels over the next few months.

The headline US retail sales data was slightly stronger than expected with a 1.4% increase for October. The September data was revised weaker to show a 2.3% decline while the core data was also slightly weaker than expected. There were further doubts over the strength of consumer spending as underlying stresses persist.

Fed Chairman Bernanke stated on Monday that the central bank would pay close attention to the implications of changes in the value of the dollar. This was a fairly forthright comment from Bernanke and does signal increased Fed and Administration unease over the dollar’s value. The US currency made initial gains, but could not sustain the advance. Bernanke also remained cautious over the economy and repeated comments that interest rates would stay low for a prolonged period.

There were no major Euro-zone economic data releases over the week. Structural fears were a focus with internal bond-yield spreads widening, notably for Greece.

There was a trade surplus for September as exports recorded firm growth and this will help ease any fears that Euro-zone competitiveness is a major issue. Euro-group head Juncker stated that the Euro was not yet at a problematic level which will dampen expectations of any action to curb Euro gains.

Nevertheless, ECB President made pointed remarks, backing Fed Chairman Bernanke’s comments on the dollar and this clearly indicates that the main central banks are more concerned over the dollar situation.

The dollar was trapped within narrow ranges against the yen over the week, but there was a slightly weaker bias with lows near 88.50. The Japanese currency also gained some support on the crosses as it tested 200-day moving averages against the Euro.

Significantly, 6-month dollar Libor rates dipped to below the equivalent yen rates which will tend to undermine support for the US currency.

Sterling was unable to sustain its best levels over the week with a retreat back to near 0.90 against the Euro and selling pressure above 1.68 against the dollar and support levels near 1.66 against the dollar broke on Friday.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are nearly 80% accurate*. 800-732-5407

If you would rather have the recent forecasts sent to you, please go here.

The latest government borrowing data was much worse than expected with a GBP11.4bn for October compared with expectations of a GBP6.1bn figure For the first half of the year fiscal year, the borrowing requirement was GBP85.9bn compared with GBP33.9bn last year. Tax receipts fell 9.1% while spending rose 10.3% over the year. The data maintained longer-term fears over the debt position

The consumer inflation data was in line with market expectations with a headline increase to 1.5% from 1.1% as transport costs increased. The data reinforced market expectations that the inflation rate has hit a low point.

The Bank of England minutes recorded a split vote at the November meeting with 1 member voting for a bigger increase in quantitative easing to GBP215bn while another member wanted no increase in the bond-buying programme. There was a unanimous vote to leave interest rates at 0.50%.

The minutes did not add much to the current debate on interest rates with the data remaining under close scrutiny over the next few weeks. The bank did discuss cutting interest rates on bank deposits which was a negative factor for Sterling. There was also a mood of uncertainty which tended to dampen confidence.