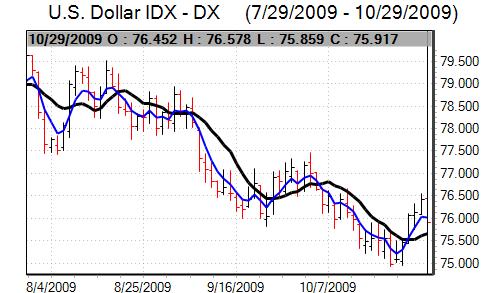

Degrees of risk appetite remained an important influence on global markets during the week. The dollar found support weaker than 1.5050 against the Euro and staged a cautious rally as risk appetite deteriorated, but gains quickly encountered significant selling pressure as underlying confidence remained weak.

US new home sales declining to an annual rate of 402,00 from a downwardly-revised 417,000 the previous month. There was a drop in inventories for the month with the number of un-sold homes at the lowest level sine August 1982 while the house-price index also rose for the fourth successive month. Nevertheless, there were further fears over the housing outlook, especially with tax credits for first-time purchases due to expire during November.

The consumer confidence data was significantly weaker than expected with a decline to 47.7 for October from a revised 53.4 the previous month. There was a deterioration in confidence surrounding current conditions and expectations with the current index at a record low as confidence in the labour market deteriorated. This development was slightly surprising given that the weekly jobless claims data has generally improved and suggested that hiring patterns are particularly weak.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are nearly 80% accurate*. 800-732-5407

If you would rather have the recent forecasts sent to you, please go here.

Risk appetite deteriorated again following the housing data as Wall Street dipped significantly with particular pressure on the Nasdaq index. In response, the Euro weakened to lows near 1.47.

The GDP report was slightly stronger than expected with a reading of 3.5% for the third quarter following a 0.7% contraction for the previous 3 months. The breakdown was broadly in line with expectations as strong buying for autos boosted the economy.

There was also a positive reading for housing investment, but there was a further contraction in business investment which will maintain unease over underlying trends. There will also still be important doubts whether the return to growth will be sustainable, especially with credit supply still contracting.

The net impact was still an improvement in risk appetite which curbed defensive demand for the US currency. There was some further speculation that the Federal Reserve will tighten its policy rhetoric at next week’s FOMC meeting, but the dollar struggled to derive much support.

Annual Euro-zone money supply growth slowed to 1.8% in September from 2.6% previously while there was a 0.3% contraction in bank lending. The persistent slowdown in monetary growth over the past few months increased fears over a credit crunch within the banking sector and maintained pressure for a loose ECB monetary policy to be maintained to help support the economy.

The latest German consumer confidence data recorded a decline for the first time in 14 months. In contrast, there was a further recovery in Euro-zone business confidence for October while the German unemployment data was also stronger than expected with a seasonally-adjusted decline for the month which helped stem immediate fears surrounding the Euro-zone economy.

ECB member Weber stated that the bank would probably start to withdraw some of the emergency measures during 2010, although he was still generally cautious over the economic outlook.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are nearly 80% accurate*. 800-732-5407

If you would rather have the recent forecasts sent to you, please go here.

The yen did secure some important support when risk appetite deteriorated, but found it difficult to sustain gains as confidence rebounded following the US GDP report. In general, it was trapped within a 90 – 92 range against the dollar. The Euro was hampered on Friday by renewed speculation that the Swiss national Bank had intervened to weaken the Swiss currency.

Commodity-related currencies dipped very sharply in the middle of the week with an Australian dollar retreat to below the 0.90 level before staging a cautious recovery as risk appetite stabilised.

The Bank of Japan held interest rates at 0.1%. The corporate funding scheme will be extended for the next three months. There was, however, a significant Bank of Japan policy move with an announcement that the commercial-paper buying programme would end from December.

The latest UK CBI retail sales survey was slightly stronger than expected with a reading of 8 for October from 3 the previous month while retailers were also confident over the outlook for November with the strongest reading for two years. The data helped underpin confidence to some extent, although the main feature was uncertainty, especially as survey evidence has been contradicted by the actual data releases.

The data on UK mortgage approvals was slightly stronger than expected with an increase to 56, 200 for September from a revised 53,000 the previous month which maintained some degree of cautious optimism towards the housing sector and the Nationwide reported a further increase in house prices.

In contrast, there was another weak outcome for consumer credit with the third successive monthly contraction. There was also a weak figure for M4 lending with the Bank of England’s preferred measures recording an annual decline. The lack of credit demand and supply will remain a key barrier to sustainable growth in the economy.

There were dovish comments from former Bank of England member Blanchflower who stated that the central bank should increase the amount of quantitative easing. There was further speculation that the Bank of England will increase its quantitative target next week, although uncertainty remained a key feature.

Sterling was able to resist selling pressure during the week and secured a significant net advance as a whole. There was a particularly robust performance against the Euro with gains through the 0.90 level while there were gains to above 1.65 against the dollar.