Markets were faced with a wide range of variables during the week as the global economy and policy responses were under close scrutiny. The dollar generally remained under pressure during the first half of the week as rallies quickly attracted selling pressure. The US currency dipped to fresh 2009 lows on a trade-weighted index and against the Euro before finding some respite.

There was further speculation that G20 would push for the US to boost savings levels in order to help curb global imbalances and would also push for a weaker dollar to boost US exports. An increased savings ratio would, however, also provide structural dollar support, at least in the medium term. There also appears very little incentive for major economies to push for a weaker US currency.

The US initial jobless claims data was slightly better than expected with a dip to 530,000 in the latest week from a revised 551,000, the lowest figure since July.

In contrast, the existing home sales data was weaker than expected with a decline to an annual rate of 5.10mn for August from 5.24mn previously. Prices continued to edge lower over the month, although there was a decline in inventories to below 9 months supply. The decline in home sales helped spark a deterioration in risk appetite which stemmed dollar selling.

The Federal Reserve and other major central banks announced that they would lessen the amount of auctions to supply global dollar liquidity. Although this suggests an improvement in credit conditions, the net supply of dollars will also tend to decline which should provide some degree of technical dollar support.

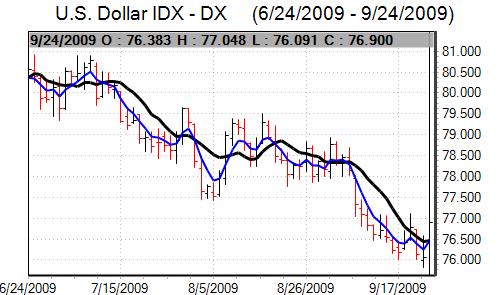

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are nearly 80% accurate*. 800-732-5407

If you would rather have the recent forecasts sent to you, please go here.

As expected, the Federal Reserve held interest rates in the 0.00 – 0.25% range following the latest FOMC meeting. The Fed stated that the economy had picked up following a severe downturn. Policy actions would contribute to a gradual recovery, but that the economy is liable to remain weak. In this context, the Fed expects interest rates to be at very low levels for an extended period. The total amount of bond buying was left on hold, but the period will be extended to the end of the first quarter so the rate of bond purchases will slow.

The Euro-zone PMI indices continued to register improvement for September with the services-sector index rising to 50.6 from 49.9, although the manufacturing-sector index stayed below the 50.0 threshold and was also weaker than expected.

The German IFO index rose to 91.3 in September from 90.5 the previous month. The advance was weaker than expected by the markets while Institute officials were generally very cautious over the outlook. The data as a whole was, therefore, a small net negative for the Euro on fears that economic improvement could stall quickly.

In comments on Tuesday, ECB member Weber stated that recent currency moves were not out of line with Euro-zone fundamentals which did not suggest significant alarm. There were, however, comments from a French official on Wednesday expressing concern over the Euro’s level. The comments suggested that the French were looking to put down a marker and there will be greater concerns if the Euro pushes above the 1.50 region.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are nearly 80% accurate*. 800-732-5407

If you would rather have the recent forecasts sent to you, please go here.

Japanese markets were closed for the first three days of the week which tended to dampen yen moves. Finance Minster Fujii repeated his opposition to currency intervention which put some renewed upward pressure on the Japanese yen late in the week with markets testing the key 90 level against the dollar. There was further speculation of near-term capital repatriation ahead of the quarter end.

The yen also gained some support from a dip in risk appetite while weaker commodity prices contributed to corrections weaker for the Australian and Canadian dollars.

The Bank of England warned that the sustainable exchange rate may have fallen in a commentary in the latest quarterly bulletin. The bank minutes recorded a 9-0 vote for unchanged interest rates and to hold the Asset Purchase Facility at GBP175bn.

Three MPC members expressed support for a larger package of quantitative easing, but decided to vote with the majority. The bank was slightly more confident over the outlook and warned over the potential medium-term inflation risks, but also still pointed to important downside risks for the economy.

Sterling came under renewed pressure on Thursday following reported comments in a newspaper interview by Bank of England Governor King that the Sterling decline will help rebalance the UK economy. Although similar comments had been made previously, the remarks reinforced market perceptions that the central bank was happy to see a weaker currency, especially after the comments within the quarterly bulletin.

Such a perception can be very dangerous for a currency, especially as markets are already very uneasy over the UK fundamentals with a continuing focus on very high government borrowing levels.

There was a much more decisive tone towards selling later in the week. The UK currency dipped to lows below 1.60 against the dollar before some respite and was also at the lowest level against the Euro since early April with lows beyond 0.9150.