Brazilian Supply Still Months Away, Near Term Tightness Should Support

By: James Cordier, Michael Gross, OptionSellers.com

The cyclical nature of agricultural markets should never be underestimated. Daily news stories, currency fluctuations and technical indicators can sway markets for sure. However, for investors concerned with long term overall direction, it would be a mistake not to at least be aware of seasonal harvest cycle ebbs and flows.

Soybeans are a market where cyclical price tendencies can play a major role.

Springtime in the Northern Hemisphere brings planting season in the world’s second largest soybean producer – the United States. However, this is also the time when the world’s largest soybean producer and exporter – Brazil – begins its autumn harvest.

Price tendencies in agricultural markets often revolve around the harvest and soybeans are no exception. Harvest time is when supplies tend to flood the market and as such, prices will often weaken to reflect the relatively high supplies.

If everything adheres to schedule this year, Brazil will begin harvesting a potentially record soybean crop in March. One would expect that this would bring price pressure to the market. But this is rarely the case. For while harvest begins in March, it is usually May or June before the bulk of beans are brought out of the fields and begin to flow into the global supply chain. Thus, soybeans will often not begin to experience harvest related price weakness until after Memorial Day.

Until that time, however, option sellers may look to the put side of soybeans as the more opportunistic play for premium collection.

For despite the fuss being made about the size of the Brazilian crop, the market will have to make do with what we have until those supplies are available. And that provides a more supportive picture for prices.

Early in the year often sees US farmers take the lion’s share of their fall harvests to market. Having held out for higher prices in the fall (which they got), the new year will often force US producers hand in unloading what is left in order to raise cash to purchase equipment and supplies for the upcoming planting season.

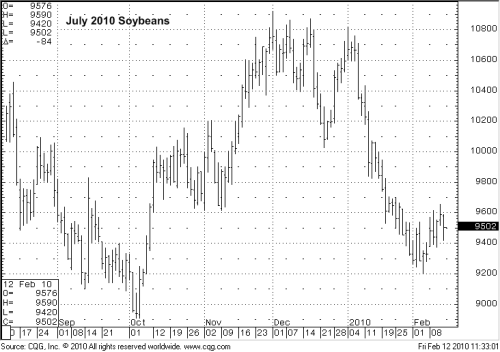

These early year marketings are what often results in the famous “February Break,” where prices “break” lower to reflect the surge in commercial selling on the cash market.

In looking at this year’s chart, it appears the “February Break” may very well have come in January. As we have stated often, seasonal analysis is rarely spot on in its timing. If farmers were eager to market early this year, (as they probably were given December’s lofty price levels) then so be it.

What this leaves the market in for the next 60-90 days is not necessarily a raging bull set up – but more of a hesitancy to sell.

With the bulk of Brazil’s beans likely not available for 90 days or more, the US is more or less the only game in town for heavy soybean importers such as China. With a large portion of the crop already gone or contracted, bids can become competitive this time of year.

Couple that with the approach of US planting season in April, and the accompanying weather jitters it often brings, and you have a market that the fund heavies are often unwilling to take short positions of any size.

This doesn’t mean prices will go higher. However, this time of year, that is often the path of least resistance.

For put sellers, having a market that is intimidating to sellers can often be just as good as a market with a strong bullish set up. Remember, you don’t need it to go up. You only need it not to fall dramatically.

The Jan/Feb price dip in soybeans could be just the right set up for put sellers this month.

That being said, the longer term set up for beans does not look overtly bullish. Despite a bullish revision in last weeks projected ending stocks in the US, the world will most likely have plenty of soybeans come June.

Brazil is expected to harvest a record 66 million tons of soybeans this year with up and comer Argentinaexpected to add another 52 million tons – also a record. Global 2010 ending stocks at 59.8 million tons would, if realized, be the second highest stocks on record. The 2010 global stocks to usage at 25.5% would be a burden to upward price movement this summer.

This set up, barring US planting problems this spring, will most likely favor call sellers by mid-year.

However, they have to get the beans out of the field first.

Until they do, look to collect your premium underneath the market. As always, we will be positioning client portfolios in deep out of the money strikes in the back months with the objective of taking profits in 60-90 days.

To learn more about selling options in the commodities markets, feel free to visit us on the web at www.OptionSellers.com. A complimentary option selling information pack is available for qualified investors.