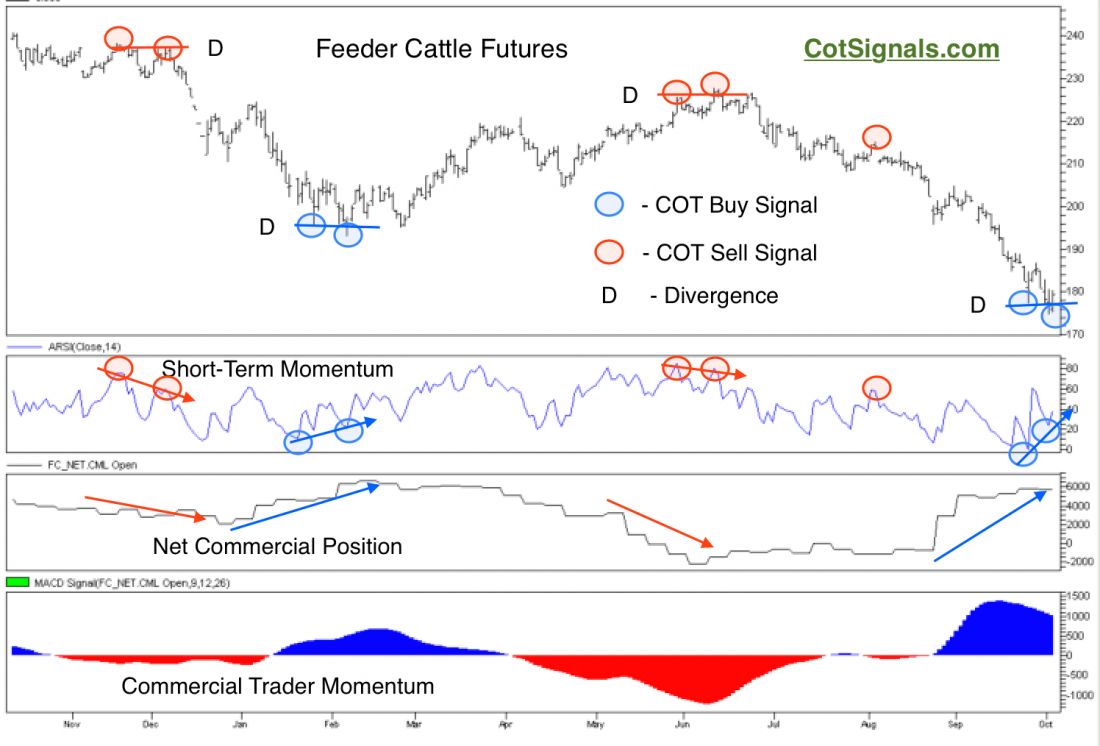

Feeder cattle futures rarely get much attention due to the live cattle futures contract. Live cattle futures have nearly ten times the open interest, therefore, the bulk of the large trading, whether speculative or hedging is done through the live cattle market. Individual traders however, can benefit by taking advantage of the feeder cattle contract’s greater size and volatility as long contract execution size is kept in the proper perspective. One of the keys I’ve found is the lower volume derivative contracts can actually provide cleaner signals than the root product. I demonstrated this a few years ago, comparing commodity trading signals to their ETF counterparts and hope to expand on this considerably next year. The current setup in the feeder cattle market is much cleaner than the live cattle market developments and illustrates one of our favorite entry techniques.

The chart below contains lots of information as it provides several textbook examples in a single snapshot. There are two types of trades on the chart, all of which are derived by the same methodology. Every circle on the feeder cattle chart represents a trading signal, five short sales and four buying opportunities including the current setup. Three of these signals are labeled as, “Divergent.” Divergent signals occur when a recent high or low is breached in price but not confirmed by a corresponding breach in our short-term momentum indicator. The new high or low in price is not confirmed by a new high or low in momentum. Most importantly for our application, each observed divergence was accompanied increased commercial trader activity in favor of the market’s reversal. These are highlighted by the red and blue arrows in the, “Net Commercial Position” portion of the chart.

Obviously, the initial signal in each of these three cases was potentially stopped out at a loss depending on the individual’s holding period. However, the second signal, which is accompanied by the divergence confirmation, ended up marking the high or low for multiple months.

This brings us to the current situation. Obviously, buying November feeder cattle on September 24th was a losing trade. Friday’s trade failed to make a new low beyond Thursday’s dive. Furthermore, Friday’s strong close triggered the bounce in our short-term momentum indicator creating the divergence. Finally, Friday was an, “inside” day. Both Friday’s high and low were below and above Thursday’s, respectively. The textbook trade here is to place an entry buy stop at Thursday’s high of $180.45. This would start the reversal higher. If the entry buy stop is filled at Thursday’s high, a protective sell stop should be placed at Friday’s low of, $175.025. That’s a risk of $2,712.50 per contract before slippage or commissions. We see first resistance of $195, which provides nearly 3 to 1, risk to reward ratio if the commercial traders are correct on their current call.