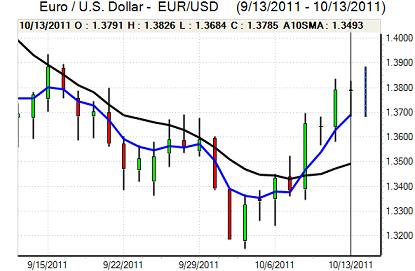

EUR/USD

The Euro hit resistance above 1.38 against the dollar in early Europe on Thursday and dipped weaker during the session with lows below 1.37 as markets took a more cautious attitude towards risk.

There was further speculation that there would be a much deeper restructuring of Greek debt with the possibility of haircuts of at least 60%. The ECB warned that any move to force private bondholders to accept bigger losses could weaken the banking sector and cause further stresses. Bank President Trichet also warned that the ECB was near its limit and could not be used as a lender of last resort.

Overall confidence in the banking sector weakened again as there were sharp losses in European share prices and this also put the Euro under pressure as there was only a lacklustre Italian debt auction result. The French government called for the EFSF to be made into a bank, but this was opposed by Germany

There was more positive news during the US session as Slovakia finally approved changes to the EFSF. Markets will then move on to unease over EFSF funding and the political difficulties in securing any further changes to the EU constitution.

The US trade deficit was marginally lower than expected, unchanged at US$45.6bn for the month as exports were marginally lower. The monthly trade deficit with China increased to a record US$29bn which will tend to inflame congressional anger over the Chinese yuan and trade tensions remained an important influence. Elsewhere, jobless claims were little changed at 404,000 in the latest week and provided some underlying dollar support.

The Euro found support below 1.37 and edged back to the 1.38 area as there was firm buying support on dips. The currency was unable to regain momentum and temporarily slid again following Standard & Poor’s downgrading of Spain to AA-.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate* 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The dollar was unable to sustain the gains seen during Wednesday’s US session and retreated back to the 76.80 area during the day. US Treasury yields edged slightly lower which dampened support for the US currency.

There was some further speculation that Japan could push for a minimum dollar rate against the yen, in a similar response to the Swiss move last month and this did have some impact in curbing yen demand at higher levels.

The currency still gained some protection from a more cautious tone surrounding risk appetite. There was some relief that China’s inflation rate fell to 6.1% for September which curbed defensive yen demand to some extent and the dollar found firm support in the 76.80 area.

Sterling

Sterling was initially blocked in the 1.5760 area against the dollar on Thursday and dipped to lows around 1.5675 before recovering ground.

The latest UK trade data was better than expected as the goods deficit narrowed to GBP7.bn for August from a revised 8.2bn the previous month. Exports were at a record level which triggered slightly more optimistic stance towards the economy despite fears over consumer spending. Any rebalancing in growth towards exports would be vital in improving the medium-term outlook.

There was speculation that the UK bank ratings would be downgraded by Fitch and there was also a market rumour of a sovereign downgrade.

Sterling proved resilient despite the negative speculation and climbed back to highs above 1.5760 late in the New York session. There was some evidence of reserve diversification underpinning the currency and its independent position outside the Euro-zone was, for now, providing support.

Swiss franc

The dollar was able to regain the 0.90 level against the franc on Thursday as risk conditions became less favourable, but it was unable to sustain the gains and retreated back below this level later in New York. The Euro was unable to regain the 1.24 level as underlying franc selling eased slightly. The dollar’s inability to hold above the 0.90 level has lessened underlying support for the currency.

Markets are still trying to adjust to the new currency regime as the franc no longer serves as a proxy for risk sentiment and volatility is likely to remain an important feature.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate* 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Australian dollar

There was further choppy trading conditions during Thursday as the Australian dollar initially lost support and retreated back to near 1.01 against the US currency before rallying again later in the New York session.

The currency was initially hampered by a deterioration in risk appetite, but there was solid buying support on dips as markets wanted to take a more optimistic stance towards the currency. A moderation in China’s inflation rate increased hopes that a soft landing can be engineered for the economy and this helped underpin the Australian dollar, although resistance was still tough to break above 1.02.