EUR/USD

The Euro was subjected to renewed selling pressure in Asia on Tuesday as risk appetite deteriorated again and underlying sentiment remained weak. The German IFO index was firmer than expected with a rise to 95.8 for January from 94.6 previously, but the Euro was unable to gain much support from the data as underlying stresses continued.

The latest US consumer confidence data was stronger than expected with a 16-month high of 55.9 for January from a revised 53.6 the previous month which will maintain some hopes over steady tone in consumer spending.

The housing data was mixed with the national data recording a small increase in prices for November, while the Case-Shiller data suggested that momentum was stalling with prices edging lower for November and October. Underlying confidence in the economy will remain fragile with continuing fears over the durability of the current recovery

The Federal Reserve will need to take a significantly tougher stance on interest rates at Wednesday’s FOMC meeting for the dollar to gain strong support on yield grounds. The most likely outcome is that the Fed will sanction only a limited shift in rhetoric following the meeting, especially with a diversity of opinion within the FOMC.

The dollar gained some support from President Obama’s proposals to curb the US budget deficit, although there are still major barriers to any fiscal package. The Euro drifted to a low below 1.4050 before consolidating around 1.4070.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate* 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The Bank of Japan left interest rates at 0.1% following the latest council meeting. It maintained an easing bias for policy, but was slightly less concerned over the deflation outlook. There will still be pressure on the bank to resist further yen appreciation given underlying weakness in the economy. The yen was also undermined to some extent by Standard & Poor’s decision to put Japan’s credit rating on negative watch

Risk appetite weakened again during Tuesday on speculation over further monetary tightening by the Chinese authorities as there were reports of further restrictions on bank lending. With equity markets also under pressure, the yen gained defensive support and the dollar weakened back to below the 90 level with a low near 89.55 before a tentative dollar recovery. The Euro also weakened to 7-month lows near 126 against the Japanese currency.

The US currency dipped lower again in US trading, but did find some support below the 89.50 level.

Sterling

Sterling held firm ahead of Tuesday’s key data release, but hit resistance above the 1.6250 level against the dollar.

The GDP data was weaker than expected on Tuesday with a reported expansion of 0.1% for the fourth quarter compared with expectations of a 0.4% expansion. The data will reinforce expectations that the economic recovery will be subdued and very fragile during 2010.

As well as the direct impact, there will also be fears that weaker than expected growth will reinforce upward pressure on the budget deficit which will tend to undermine Sterling support, especially given the degree of market unease already. The latest mortgage approvals data was also weaker than expected which reinforced fears over the economic outlook.

The UK currency dipped sharply following the GDP data, but did find support below the 1.61 level against the dollar and consolidated above this level.

Swiss franc

The dollar found support below 1.04 against the Swiss franc and pushed to a high near 1.05 before retreating to the 1.0450 level in New York. The Euro held just above 1.47 against the Swiss currency during the day with no reports of National Bank intervention.

There will be persistent fears over the Euro-zone outlook which will continue to provide defensive support for the Swiss currency.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate* 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

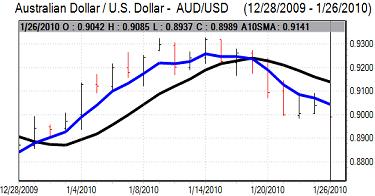

Australian dollar

The Australian dollar was subjected to renewed selling pressure in Asian trading on Tuesday with lows just below 0.8950 against the US dollar. Risk appetite deteriorated again on fears that there would be further Chinese monetary policy tightening over the next few weeks and overall confidence surrounding the global economy was fragile.

The currency resisted further losses during the day and edged higher to the 0.90 level later in the US trading session before hitting tough resistance.