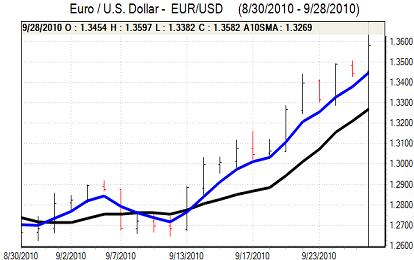

EUR/USD

There was little change in Asian trading on Tuesday. There were media reports that the Fed would adopt a more limited form of quantitative easing which stemmed dollar selling, but there was no strong support for the US currency given the weak fundamentals.

There were renewed doubts surrounding the Euro-zone financial sector in European trading and the Euro dipped to test support below 1.34. It found support below this level and the remainder of the day was dominated by dollar weakness.

There were reports from a Chinese official that dollar devaluation was inevitable in the longer term and there were also some supportive comments surrounding Euro bonds which undermined the US currency.

The US housing data was slightly weaker than expected with the Case-Shiller house-price index registering a 3.2% annual increase from 4.2% the previous month. The consumer confidence data was significantly weaker than expected with a decline to 48.5 in September from 53.2 previously and this was the lowest figure since February. With consumers pessimistic over the employment outlook, overall confidence in the economy and dollar weakened significantly.

After a brief respite, there was also renewed speculation over a Fed move to boost quantitative easing with reports that the Fed would decide on such a policy change at the early-November FOMC meeting. In this environment, the dollar was subjected to heavy selling pressure and weakened to a 5-month low near 1.36 after important resistance near 1.35 was broken.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The yen was little changed in Asian trading on Tuesday with the Japanese currency restrained by speculation that the Bank of Japan could adopt further quantitative easing at next week’s monetary policy meeting. Currencies which are seen as prone to further monetary action have been vulnerable and this dented safe-haven demand for the yen to some extent.

Risk appetite was slightly more cautious during the session following a decline on Wall Street which curbed yen selling and there were also some reservations of potential capital repatriation before the end of September. In this environment, the dollar held close to 84.20 against the yen in subdued trading conditions.

The dollar came under renewed selling pressure following the US economic data and there were lows near 83.70, the lowest figure since the Bank of Japan intervened earlier in September. There were no reports of central bank intervention during the session.

Sterling

There were strong Sterling moves during Tuesday and several changes of direction on very mixed influences for the UK currency.

The UK data was stronger than expected and provided initial support to the currency. Second-quarter GDP was confirmed at 1.2% while the current account deficit was lower than expected at GBP7.4bn from a revised GBP11.3bn previously.

The latest CBI retail sales survey was much stronger than expected with a rise to 49 for September from 35 the previous month and this was the highest figure since 2004.

The positive sentiment garnered from the data releases was more than offset by very dovish comments from MPC member Posen. He stated that there was a clear case for further asset purchases by the Bank of England and that inflation was likely to substantially undershoot the 2.0% target in the medium term. The comments revved speculation that the Bank of England could adopt further quantitative easing and also increased unease over wide splits within the MPC.

From a 7-week high near 1.59, Sterling weakened to near 1.57 against the dollar before settling in the middle of this range as the dollar came under pressure. Sterling weakened to a 4-month low of 0.86 against the Euro.

Swiss franc

The Euro again hit resistance close to 1.33 against the franc on Tuesday, but found support below 1.32 in choppy trading. The dollar came under fresh pressure against the franc and weakened to a fresh record low below 0.9750 against the Swiss currency.

The franc gained initial support from a lack of confidence in the Euro-zone financial sector. Although these fears eased slightly during the day, the franc continued to gain underlying support from speculation that several G7 countries would pursue additional quantitative easing.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

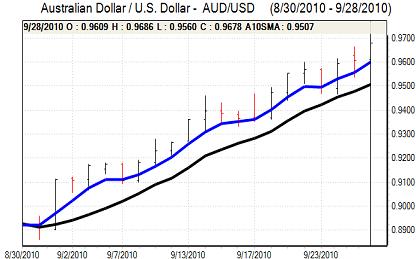

Australian dollar

The Australian dollar dipped to lows near 0.9550 against the IUS currency during Tuesday, but then found renewed support and pushed to fresh two-year highs above 0.9680 during the US session.

US currency weakness was again an important influence which underpinned the Australian currency. The speculation over fresh quantitative easing by the US Federal Reserve also provided additional support for the Australian currency as yield factors remained important.