Through the 1980s, Sears was the largest retailer in the United States. In 2018, Sears was the 31st-largest retailer in the United States. After several years of declining sales, Sears‘ parent company filed for Chapter 11 bankruptcy in October 2018. Starting in the 1990’s, the Chicago-based company had been amassing outstanding debt of around $5.6 billion. After several years of stumbling from one crisis to the next, the company was unable to meet interest payment on their debt and their leadership sought Chapter 11 protection, putting the jobs of 89,000 employees at risk.

Unfortunately, this is a very common narrative today.

Companies like Sears are referred to as Zombie companies. This is a term used to describe an uncompetitive company that needs a bailout to successfully operate or an indebted company that is unable to repay interest on their debt obligations.

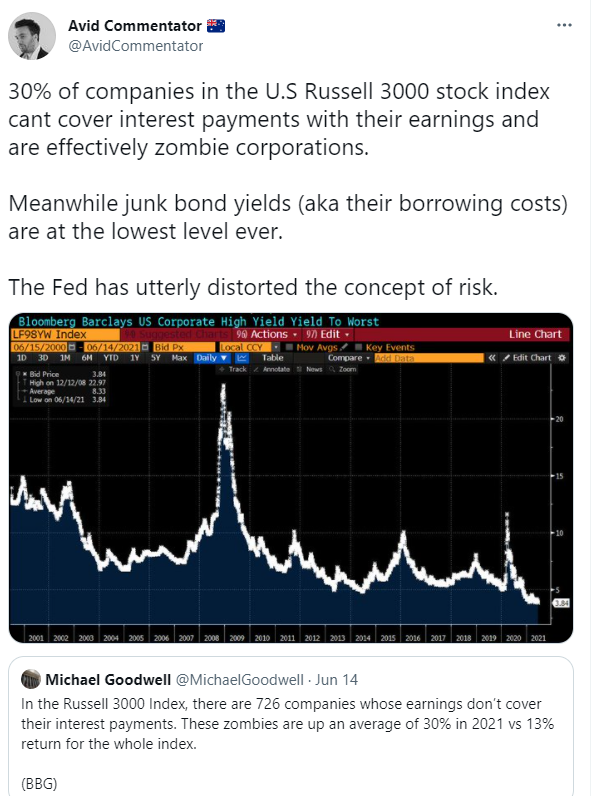

Economic slowdowns greatly increase the number of firms that meet this criterion. What is truly unusual is that share prices on the major US exchanges are hitting all-time highs at the same time the number of Zombie companies, that do not make any money at all, are rising. Currently, in the broad benchmark of U.S. stocks known as the Russell 3000 Index, there are 900 companies whose earnings do not cover their interest payments on their outstanding debt. That represents 30% of the Index. The end result of this problem is these companies rollover their debt in larger quantities at lower interest rates in an attempt to survive.

You’re familiar with these companies, AMC, Macy’s, Boeing, ADT, ROKU, the four major airlines (Delta, United, American, and Southwest), Mattel, Carnival, Exxon Mobil, and Marriott International, to name just a few. When the Zombie company employs too many people the narrative becomes “too big to fail”, like it did in the 2008 financial crises.

Why are Zombie companies proliferating? Two words.

The Fed.

The monetary policies seen over the past decade have exacerbated the Zombie company problem. The historically low interest rates, coupled with quantitative easing (QE) have helped these companies amass over $2.6 trillion in debt that they cannot service. A decade of binge borrowing has turned many corporations into the walking dead. This level of indebtedness impedes their ability to hire and continues to spur on malinvestment.

These deeply indebted companies are trying to muscle through their troubles by borrowing even more money from the Fed.

When the Federal Reserve tried to prevent a rash of bankruptcies in 2008 it purchased all of these companies’ corporate bonds. But in helping thousands of ailing companies gain virtually unfettered access to credit markets, they inadvertently directed the flow of capital to unproductive firms. Since the 2008 financial crisis the Fed has been the primary purchaser of these bonds allowing all of these companies to receive almost zero rate financing on their debt obligations.

This has been troubling me lately as I watched the Feds FOMC press conference two weeks ago. It communicated to me exactly how fragile the markets and the economy are. The market sold off 2.5% over a couple of days and the headlines read like World War 3 had just begun.

The Fed hasn’t started to end Quantitative Easing yet. They haven’t even set a date to start the taper. All they did in that press conference is state that they are beginning discussions as to when in 2023 they MIGHT begin reducing their $120 billion per month in asset purchases.

Instead of reducing debt and de-leveraging, the zombies are re-leveraging. It’s all about “free money.”

As disruptive as bankruptcy and other major debt restructurings are, they are key to freeing over-leveraged companies from their “zombie” persona and allowing capital to flow into more productive areas.

When credit markets function normally, their purpose is to assess which businesses are loan worthy and which ones truly don’t have a future. So long as the Fed and other central banks maintain this “free money” approach, the credit markets, and their function in defining risk have been hollowed out.

The distortions in price discovery have become so massive that investors are forced to trust public relations press releases more than actual results. Look at the following list of companies that are unprofitable.

Airbnb

Dropbox

Casper

Blue Apron

Lime

Lyft

Peloton

Slack

Snap

WeWork

Wayfair

Zillow

None of these are profitable but a handful of these darlings have great memes. ?

The only way to reverse this trend is to encourage innovation, re-investment, job creation, entrepreneurship, and economic output. Profitability is required for these outcomes to occur.

I know that on the surface this can sound like the ramblings of an Ebenezer Scrooge like character who shows no compassion for the misfortune and hardships of others. The reason this is important is that in capitalism, and in trading the losing side of the ledger is much more important than the winning side. Knowing what doesn’t work is what entrepreneurs’ study to be able to discover what does work, and to come closer to that innovation that sparks new growth and industry. When you perpetuate the “what doesn’t work” side of the ledger you are guaranteeing that the same costly mistakes will occur over and over again throughout the economy. In other words, there are no consequences for bad behavior or performance. The survival of Zombie companies hinders this important element of the free market, which is ‘Creative Destruction’ from evolving. This is a term developed by the economist Joseph Schumpeter which refers to the economic process of how old industries die and replaced by new, more effective, efficient businesses. It explains the process of how we went from horse and carriage to automobiles. Or how we went from floppy disk to CDs to pen drives to cloud storage. Creative destruction is how better products are created at lower prices, offering more value to the consumer. This idea argues that by continuing to support zombies we prevent the new dynamic companies from coming into creation.

If you think this sounds extreme all you have to do is look at Japan as the embodiment of this problem. The Japanese Government Bond market is the 2nd biggest bond market in the world and has a market cap of roughly $10 trillion. This market barely trades any longer as its only customer is the Japanese Central Bank. There are almost no private investors who will buy Japanese Bonds anymore. The Bank of Japan has loaded its balance sheet with Japanese debt that it forced interest rates below zero percent back in 2016; and the result is the free market has perished. The end result is that for 30 years the Japanese economy has languished. Look at the following chart of the Nikkei Index and you can see its lackluster negative performance over 30 years.

Investors do not buy Japanese Government Bonds, which are guaranteed to lose principal after adjusting for inflation. But these same investors, are not in any hurry to sell their existing bond holdings because they understand the government will be there to support bond prices.

This is tantamount to a trader refusing to take a loss on a trade and just waiting, and waiting, and waiting, and waiting for it to get back to breakeven. You have tied up your capital in a bad situation instead of being able to move it into another trade where it can be more productive.

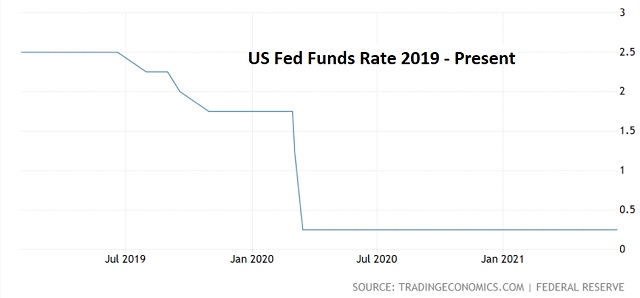

Sadly, the U.S. is headed in this exact same direction as Japan. This is why we can be certain central banks’ monetary tightening cycles won’t last for very long and will end in severe market contractions.

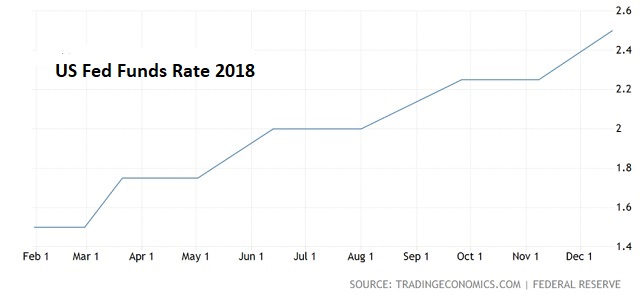

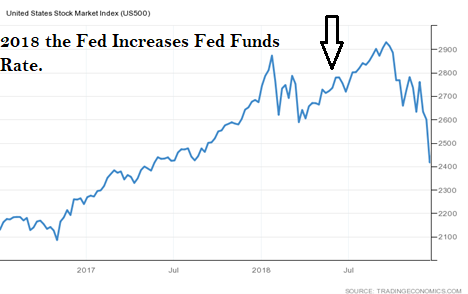

In 2018, the Fed tried to moderate its policy of low interest rates, massive money printing and purchasing of corporate and government bonds. Over a period of 10 months, it gradually raised interest rated through the U.S. Fed Funds rate 1%.

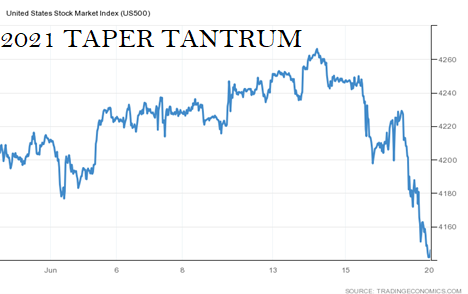

And the financial markets, which had become addicted to easy money threw what has come to be known as the 2018 “taper tantrum.”

Two weeks ago, the Fed merely suggested that in 18 to 24 months’ time they might begin scaling back their purchases of Bonds in the face of what appears to be 5% inflation and the markets once again responded with the 2021 “taper tantrum.” Keep in mind they didn’t change the Fed Funds rate. They merely talked about possibly, maybe, at some point in the distant future they might possibly consider raising it.

And so, we’ve arrived at that long-awaited monetary policy endpoint.

The Fed cannot never be able to tighten monetary policy without causing a crash in the markets.

Never.

What does this mean to you as an investor and trader?

As more and more money is being printed and the Fed continues to support financial markets it is crystal clear how fragile the economy is.

Dollars are being debased. Financial assets are increasing in price because the Fed is purchasing assets that no one else will.

While I have shared my opinion with you about what I see is the fundamental current economic environment, I want to be clear that I never let my opinion interfere with my trading decisions.

My reality is always formed by what I see, hear, feel, and understand. I have come to appreciate that what I see, hear, feel, and understand is a very small universe indeed. This is why I use artificial intelligence, neural networks, and machine learning to guide my trading decisions.

You have probably heard the old adage, that bull markets take the stairs and bear markets take the elevator.

Everybody has had horrible trades. The difference between the winners and losers in life is that the winners learned very powerful lessons from their losses.

Artificial intelligence is so powerful because it learns what doesn’t work, remembers it, and then focuses on other paths to find a solution. This is the Feedback Loop that is responsible for building the fortunes of every successful trader I know.

If you think about this question, you will begin to appreciate that ai applies mistake prevention to discover what is true and workable. Artificial Intelligence applies the mistake prevention as a continual process 24 hours a day, 365 days a year towards whatever problem it is looking to solve.

That should get you pretty excited because it is a game-changer.

It sounds very elementary and obvious. But overlooking the obvious things often hurt a traders’ portfolio.

The basics are regularly overlooked by inexperienced traders.

It is very sad, and unnecessary in today’s day and age of machine learning and artificial intelligence.

A stock may have a very alluring story.

A stock may have a very effective management team.

A stock may have incredible earnings.

A stock may have infrastructure, partnerships, uniqueness, etc.,

But, if these elements are not reflected in the price, you are focused on what “SHOULD” occur in the market.

And the word should is responsible for more losses in trading than any other.

Bad Traders Obsess on the SHOULD. Every other word out of their mouths’ is SHOULD.

I can’t recall how many times a trader has told me all of the reasons why his portfolio is heavily invested in a stock because of a great story, in spite of the stock being in a firm downtrend. It is horribly painful to listen to.

The beauty of neural networks, artificial intelligence and machine learning is that it is fundamentally focused on pattern recognition to determine the best move forward. When these technologies flash a change in forecast it is newsworthy. We often do not understand why something is occurring but that does not mean that we cannot take advantage of it.

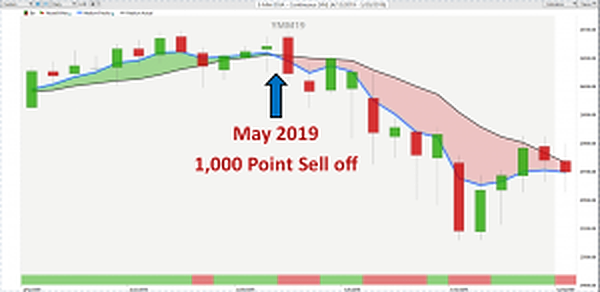

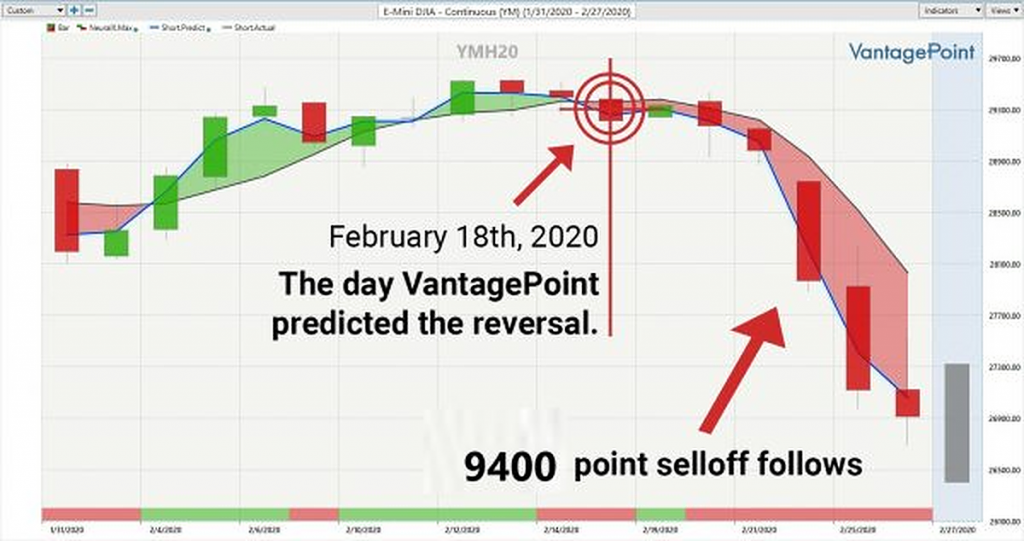

The following charts illustrate how Vantagepoint power traders READ the price action to anticipate tomorrow’s headline NEWS.

As I stated earlier, PRICE is the only thing that will make you RICH or POOR. And it is these price changes correlated to the asset classes which are most statistically relevant which are responsible for creating these trend forecasts which have proven to be 87.4% accurate.

My OPINION is that I think we are going to have a massive stock market pullback soon. But I do not let that opinion get in the way of my trading behavior. When the a.i. signals the DOWN trend forecast I will be there!

More importantly, look at how the artificial intelligence kept traders on the right side of the downtrend every step of the way.

This is the power of artificial intelligence in action.

This is what makes Artificial Intelligence so powerful and unique.

Machine Learning is designed to learn from experience and make the best statistically relevant decision moving forward. AI outperforms humanoid analysis hands down every time.

We live in very exciting times.

What hurts can instruct us.

Artificial intelligence has decimated humans at Poker, Jeopardy, Go! and Chess. Why should trading be any different?

I invite you to check it out at our Next Live Training.

It’s not magic. It’s machine learning.

Make it count.

IMPORTANT NOTICE!

THERE IS SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.