If you ask the average person about the commodity futures markets, you will usually receive one of two responses.

- A blank stare. Or,

- That they are risky.

Today, more than ever, with all the volatility and uncertainty in the economy, it’s an excellent time to learn why the commodities markets exist and how traders use them to both profit and protect the purchasing power of their portfolio.

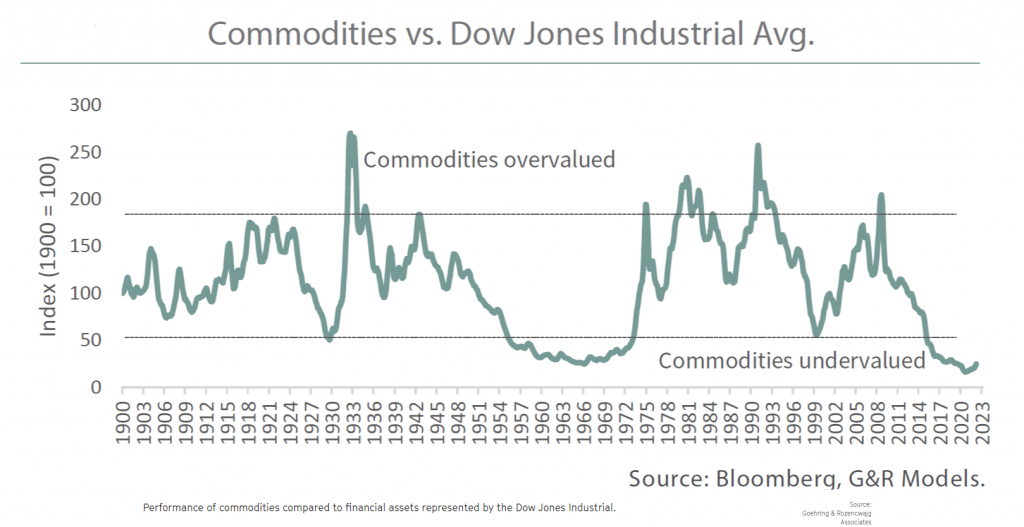

Recently, I stumbled across the following chart which captivated my attention. It’s a 120-year graphical representation that shows the relationship of the Dow Jones Industrial Average versus basic Commodity prices. Historically, commodity prices usually move inversely to the price of stocks. During periods of great economic turmoil and inflation we normally see giant increases in commodity prices. Should this relationship continue moving forward, it is clear to conclude that currently commodity prices are dramatically undervalued compared to the Dow Jones Industrials. This will create tremendous opportunity for trader who know how to manage and control their risk.

The commodity futures markets were invented in the 19th century to provide “price insurance” and hedging for farmers and other producers. By entering contracts to sell their commodities at a set price, farmers and producers could avoid the risk of price fluctuations and price declines. The futures markets also provided liquidity, making it easier for farmers and producers to buy and sell their commodities. In addition, the futures markets helped to ensure that prices remained stable, which was vital for the economy. Today, the commodity futures markets continue to play a key role in price discovery and risk management.

The commodities marketplace is remarkably diverse and consists of most products which are consumed by a modern economy.

Agriculture commodities include grains such as corn, soybeans, and wheat; livestock such as cattle, pork, and chicken; and soft commodities such as coffee, sugar, and cocoa. Energy commodities include crude oil, gasoline, natural gas, and heating oil. Metals commodities include gold, silver, copper, and platinum. Even the forex market and stock market indexes have extremely popular commodity contracts which actively trade on the exchanges. These are just a few examples of the many commodity markets that exist. In each market, prices are driven by supply and demand fundamentals. For example, droughts can lead to higher prices for agriculture commodities, while geopolitical tensions can lead to higher prices for energy commodities.

To see a listing of all of the contract listings which trade on the Chicago Mercantile Exchange you can click here.

The easiest way to understand why these markets evolved is to simply imagine that you own one billion units of any of the previously mentioned commodities. If you entertain this thought exercise you immediately understand that your risk is defined as an adverse price move.

The only way you can completely protect the entire value of what you have is to acquire price insurance by taking an equal and opposite position in the futures markets. In other words, you would sell one billion units of the commodity contracts. By doing so, you would be hedged 100%. This means that if prices declined you would lose value on your physical inventory, but you would gain value on the futures contracts which you sold short.

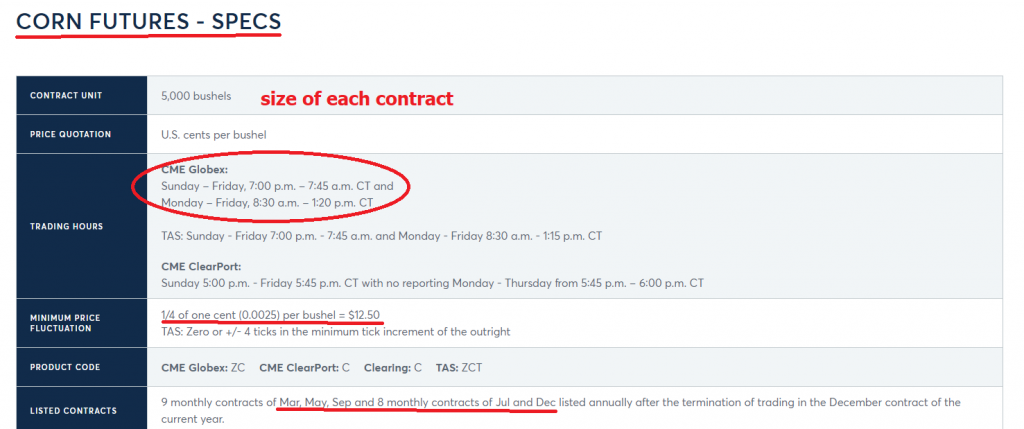

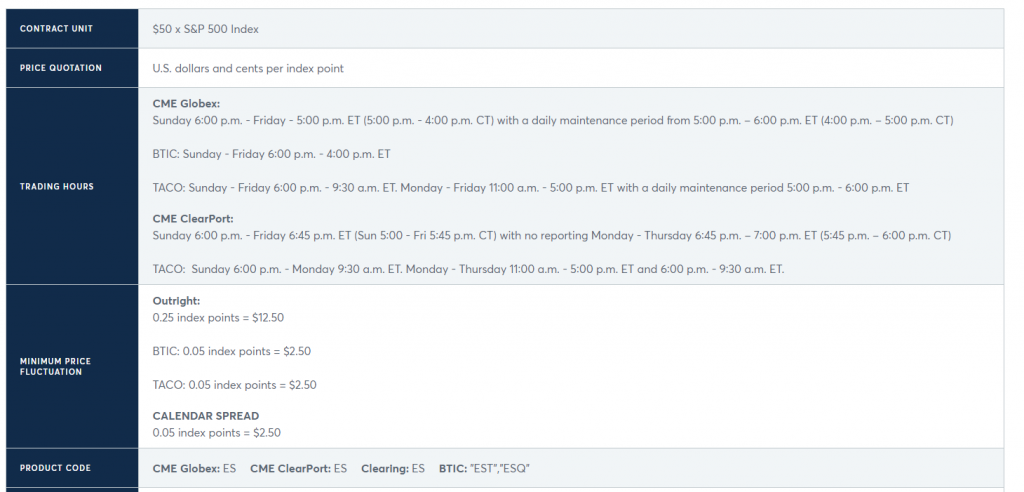

Every commodity has certain standardized features such as agreed upon trading hours, how prices are quoted, minimum price fluctuations, product quotes and symbols as well as what trading months are available for trading. These specifications are listed in the following graphic and are available for each commodity which is traded on the exchanges.

A hedger is a trader in the commodities, futures or options market who takes an equal and opposite position from his inventory to minimize his risk.

A speculator is an individual who trades in the commodities, futures, or options market for the sole purpose of profiting from price changes.

To make a profit, a hedger must be correct about the direction of the underlying commodity’s price. For example, if a corn farmer believes that the price of corn will go down, he may choose to hedge his position by selling corn futures. If the price of corn does in fact go down, he will make a profit on his futures contract and offset some of his loss on his inventory. However, if the price of corn goes up, he will lose money on his futures contract but make money on his inventory. A speculator, on the other hand, would simply buy corn futures if he believed that the price of corn was going to go up. If the price of corn goes up, he will make a profit on his contract. If the price of corn goes down, he will lose money on his contract.

Producers of commodities are not in the business of speculating on price. Producers of commodities attempt to control their costs when producing the commodity and in doing so, they try to liquidate their inventory shortly after it is produced to earn a small profit if they are successful.

Speculators on the other hand are integral to the operation of the futures markets. They are traders, large and small who provide liquidity for the marketplace as they position themselves long and short in anticipation of price changes.

To make this example as realistic as possible for stock traders, let’s look at the E-Mini S&P 500 Futures contract. This futures contract has a market value of $50 times the value of the S&P 500 index. Currently, the S&P 500 Index is trading at 4,000. So, the entire cash value of the contract is $200,000.

When you trade commodity contracts, you are required to post a good faith deposit, or margin, to open the trade. This deposit is a small percentage of the full value of the contract and is used to ensure that you can meet your financial obligations in the event of an adverse price movement. The amount of margin required varies depending on the commodity and the exchange but is typically around 5-10% of the value of the contract.

If the market moves against your position and your account equity falls below a certain level, you will receive a margin call from your broker. At this point, you will be required to deposit additional funds to maintain your position. If you are unable to do so, your position will be closed out at whatever price is available in the market. As such, it is important to always have adequate funds available to meet any margin calls that may arise.

But here is where the rubber meets the road. The cash value of this futures contract at the present time is $200,000. What makes trading futures contracts risky is the amount of leverage that you receive if you should choose to take it.

For example, the most leverage you can receive trading stocks is roughly 50%. This is done by the brokerage company loaning you 100% of the value of your portfolio so that you can purchase more stocks. In Commodities and futures, there are no loans. Instead, you place a good faith deposit, referred to as margin and you can trade the underlying futures or commodity contract. The good faith deposit required to trade the E-Mini S&P 500 Futures contract is $10,500. In other words, you control $200,000 worth of stocks with a deposit of $10.500. The margin requirement represents 5.25% of the cash value of the contract. If the price goes up 5.25% on the S&P a speculator has made 100% on their good faith deposit. But the same can be said about a a price decline. Should prices move 5.25% lower, a speculator would have lost 100% of their margin requirement. Since the S&P 500 Index declined over 24% since the beginning of the year you can imagine the losses that commodity speculators incurred if they were trading on minimum margin requirements.

Risk and leverage are the same. The more leverage you incur the greatest the risk you are taking. Commodity markets in and of themselves are no riskier than trading stocks. On average they move a small amount every day. But these moves result in exponential gains or losses since the traders involved in these markets have deposited small margin amounts to be able to open their positions.

The reason this amount of leverage exists is to provide massive liquidity to producers who are looking to hedge their inventories. For example, let’s say you have a portfolio of ETF’s that are highly correlated to the S&P 500 Index. If you were uncertain about future market conditions you could simply hold your cash position in stocks and ETF’s and sell short 1 e-mini-S&P 500 futures contract, and not have to produce the full contract value to be hedged. By doing so, you would be acquiring price insurance against an adverse price movement. You would make money on your short futures position and lose money on your cash etf position.

Today because of the increased volatility in many assets and the instantaneous transmission of information, prices move faster than ever before. Professionals understand how important hedging can be, particularly when dangerous market conditions arise.

We have experienced HUGE inflationary pressures in the economy. In time this traditionally results in significantly higher commodity prices. For traders who are seasoned risk managers, this can be an ideal opportunity for future profitability. Now is a perfect time to study the opportunity of learning how to trade commodities.

When it comes to trading commodities futures contracts, the best way to learn is to paper trade or use a demo account. This will allow you to get a feel for the market without risking any real money. You should also only trade with money that you can afford to lose. This way, even if you make some bad trades, you won’t end up in financial trouble. Finally, be sure to keep your emotions in check. Trading can be exciting, but it’s important to stay calm and rational. If you let your emotions get the better of you, it’s extremely easy to make costly mistakes. You want to make sure that your paper trading strategy is sound before risking actual money.

What does this all mean for you the trader? Over the past two and a half years we have seen an unprecedented increase in the Money Supply. As inflation rears its ugly face, you can anticipate that the end result will be that prices will change very quickly.

And with higher volatility comes greater opportunity for traders who know how to locate opportunities.

But to be effective in markets you need to drill down to always strive to be on the right side, of the right market at the right time.

Great traders are obsessed with not losing money. Having a repeatable discipline to uncover great trade ideas is vital to today’s giant market distortions.

This is why neural networks, machine learning, and artificial intelligence are a necessity for today’s trader. When what “SHOULD” happen aligns with what “IS” happening some pretty explosive outcomes can occur and that is where you want to be as a trader. That is the promise of artificial intelligence can make to you today.

The challenge of trading is the organization of information so that effective decision-making can occur. How good have your decisions been over the past year? How do you think your trading decisions compare to A.I.?

Mistakes are problematic for humans, but for machine learning it’s the pathway to mastery and excellence. The real education in trading always lies in learning from the losers and completely understanding why something doesn’t work. More importantly, as a trader you want to focus your hard-earned savings on what is proven to work.

Most humans have a tough time learning from bad experiences. The ego gets in the way, each and every time.

Since artificial intelligence has beaten humans in Poker, Chess, Jeopardy and Go! do you really think trading is any different?

Moving forward I want you to think long and hard about HOW you are going to trade the markets if you do not have an edge. As the volatility of the past few months becomes commonplace are you prepared?

Think about those losing trades and ask yourself what did you learn from that experience? What is your method for analyzing risk?

Knowledge. Useful knowledge. And its application is what A.I. delivers.

Artificial intelligence is not “a would be nice to have” tool.

It is an “absolutely must have” tool to flourish in today’s global markets.

We live in exciting times.

What hurts can instruct us.

Mistakes are financially costly but for machine learning, it is the pathway to mastery and excellence. The real education in trading always lies in learning from the losers.

Visit with us and check out the A.I. at our Next Live Training.

It’s not magic. It’s machine learning.

Make it count.

IMPORTANT NOTICE!

THERE IS SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.