With volatility ramping higher, relative value and pairs trading methodologies offer the potential prospect of higher returns with lower risk than buy and hold. When it comes to the ETF world, there are three ways to play this. The first is to find near substitutes to arbitrage occasional statistical mispricings. The second is to find pairs that offer varying beta levels, then fade the differentials. The first is obviously the safer, albeit rarer of the two, yet both can be profitable as long as traders are aware of the risks they may be taking with the later method which nevertheless requires consistent volatility to “work”. The third method is to trade ETFs against baskets of individual stocks, which goes beyond the scope of this post.

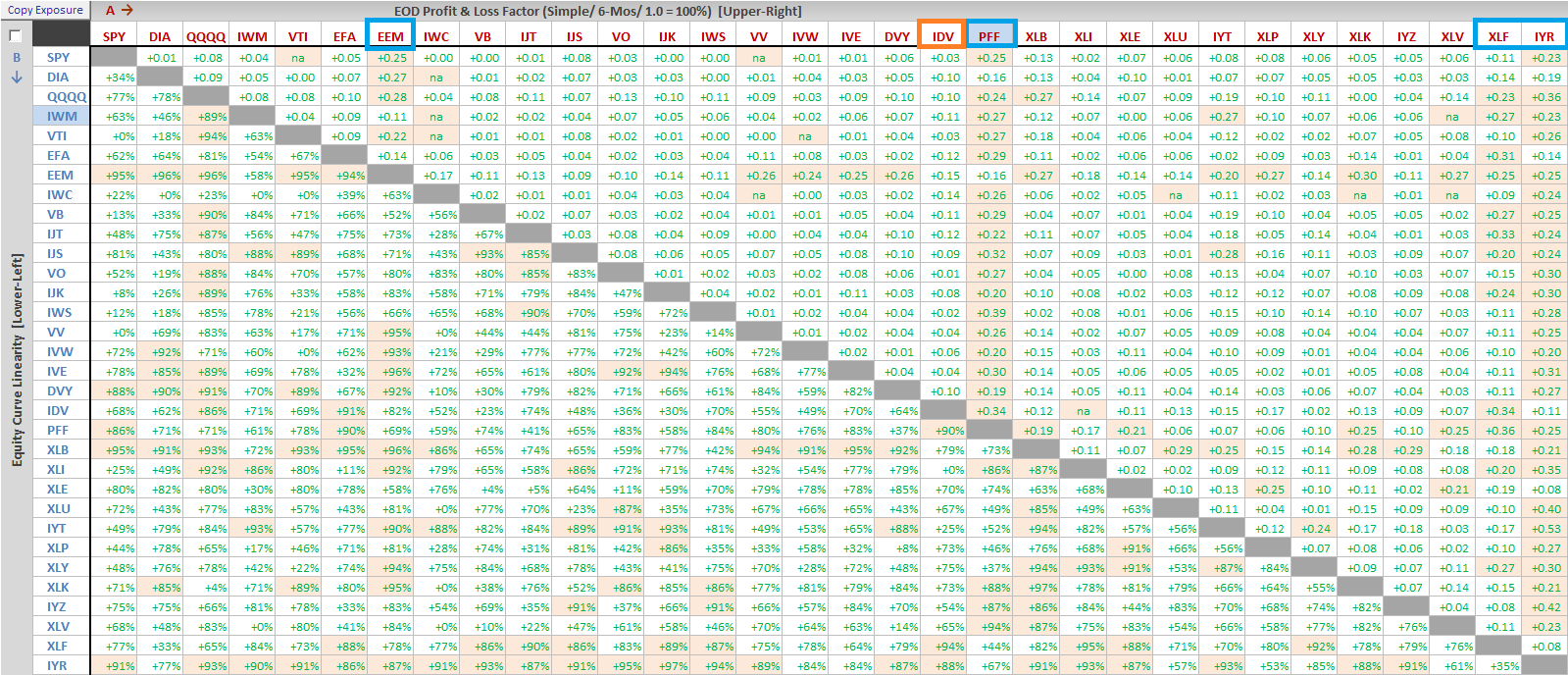

The table below investigates potential profitability of the second beta offset method using cross pairings of 32 major indices, capitalization and styles, and major sectors. The upper-right hand cells provides hypothetical end-of-day profit and loss results for the various pairings after trading costs using optimized parameters, while the lower-left hand area shows the linearity of those return series.

The circled ETFs offered the most consistently high return pairings, including EEM, PFF, XLF and IYR. Since this run only covered the most recent six month period, I also went back to May of 2009 to capture the volatility peak, where the same cast of characters arose with the addition of IDV. More interesting results may be achieved looking at Countries and Subsectors. This entire analysis was conducted using the standard tools provided in the nightly ETF Rewind worksheet.

[Related: More on Pairs Trading]