After a decisive trend last week with the dollar under pressure, the moves this week were initially less clear as wider uncertainty over economic and policy trends contributed to indecisive currency trading, especially with pressure for a consolidation. Risk appetite remained an important feature and confidence was generally weaker later in the week. This was most obvious in the fact that 1-month Treasury bill yields fell below zero for the first time since December.

The US Treasury announced over the weekend plans to use US$75-100bn of TARP funds in combination with private capital to boost the potential for troubled assets to be cleared. The Administration will effectively provide a discount for private-sector purchasing of assets with guarantees provided by the FDIC. There was a generally favourable reaction with strong Wall Street gains.

The issues of reserve currencies and exchange rate management were again important influences following recent comments from China over the possibility of greater use of an alternative reserve currency such as the SDR

Treasury Secretary Geithner initially stated that the Administration was open to the idea which weakened the dollar sharply, although he then made a series of clarifications that the dollar would remain the dominant reserve currency.

The US economic data recorded an increase in existing home sales to an annual rate of 4.72mn in February from 4.49mn the previous month. Activity was stimulated by lower costs as prices fell by over 15% over the year while inventories remained historically very high. New home sales also rose to an annualised rate of 337,000 for February from a revised 322,000. Durable goods orders also recorded the first increase for seven months.

Initial jobless claims increased by slightly more than expected to 652,000 in the latest week from 644,000 previously. Continuing claims rose to a fresh record high of 5.56mn which suggested that it is still very difficult to find new employment.

The PMI surveys recorded a small monthly improvement in headline indices for March which suggested that activity may be stabilising to some extent, although the employment data remained extremely weak. The German IFO index edged lower to 82.1 from 82.6 which was a fresh record low for the survey with some optimism in the construction sector while other sectors were more pessimistic

ECB members, including Chairman Trichet, have suggested that there is scope for a further reduction in interest rates, but also expressed doubts over the potential over zero rates with resistance to any further non-conventional measures.

The headline Euro-zone trade deficit increased to EUR10.5bn for January from a revised EUR1.7bn previously. Although the seasonally-adjusted deficit was lower, there was still an important deterioration as exports again weakened sharply.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 80% accurate. 800-732-5407

If you would rather have the recent forecasts sent to you, please go here.

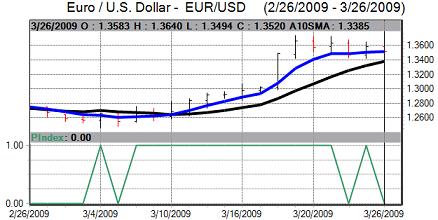

After correcting slightly weaker against the dollar, Euro losses accelerated towards 1.33 against the dollar on Friday while it also surrendered some of the gains on the crosses

The Japanese trade account returned to surplus for February for the first time in five months. The main focus was on the continuing plunge in trade volumes with exports falling 49% over the year as auto shipments fell sharply.

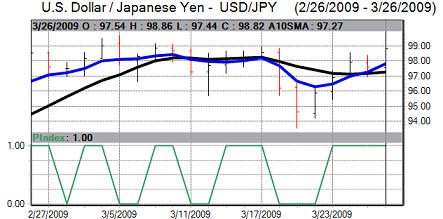

The yen was generally on the defensive over the week as rallies quickly attracted selling pressure due to a lack of confidence in the Japanese economy, but the dollar continued to hit tough resistance above 98.50 against the yen. The US currency found support below 1.12 against the Swiss franc and rallied to a high above 1.1420.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 80% accurate. 800-732-5407

If you would rather have the recent forecasts sent to you, please go here.

The UK consumer inflation rate was sharply higher than expected at 3.2% in March from 3.0% previously and compared with expectations of a drop to 2.6%. The RPI did not fall to below zero as had been expected due to higher food and transport prices. There was increased speculation that the Bank of England would be more cautious over promoting an even more aggressive monetary policy and Sterling weakness.

The Bank of England warned that the government should not boost fiscal policy further given the debt stresses and the warning undermined currency support given that fiscal fears were already an important factor.

UK retail sales fell 1.9% in February after a revised 0.8% increase the previous month and cut annual growth to 0.4%. The data undermined sentiment to some extent, although the impact was measured due to potential distortion by bad weather at the beginning of the month. The UK CBI retail sales survey was weaker than expected at -44 from -25 previously and the April expectations component was also weak

The latest gilt auction reported a bid/cover ratio below 1.00 compared with 2.03 the previous month with potential buyers unsettled by the higher than expected inflation rate reported on Tuesday. There were increased fears that the UK would not be able to attract sufficient overseas buyers for the very heavy bond issuance schedule. The current account deficit was little changed at GBP7.6bn for the fourth quarter.

After pushing to a high above 1.47 against the dollar, Sterling weakened back to lows below 1.43. The UK currency also weakened against the Euro with lows close to 0.94.