Professional traders use options as risk management instruments. This has been the case since the development of Options trading in the 1970’s. To effectively manage risk traders create risk/reward scenarios using a combination of stock options, index options and futures options. The potential danger for retail speculators is becoming the effect of these trades when they all unwind simultaneously. While the probability of this occurring is rare, there are numerous instances of when it has occurred. In this article we will explore how the these instruments can create massive volatility in the stock market.

Throughout the 1980’s and 1990 there was a phenomenon referred to as “triple witching hour.” Triple witching hour occurred four times a year, on the third Friday of March, June, September, and December. During this time, price correlations were most volatile due to simultaneous expiration of stock options, index futures, and index options. The name triple witching hour was coined as this day and time frame saw a massive unwinding of positions which increased volatility in the stock market. It was commonplace to hear media pundits discussing and warning traders about “triple witching hour.” This created heavy buy and sell activity as investors tried to take advantage of price movements caused by these key drivers. Today, such occurrences can still cause price spikes or drops within certain stocks depending on how traders’ decisions affect these instruments; however, due to increased liquidity within markets price instability mostly takes place in sectors where price correlations are lagging.

Triple witching hour today is recognized as the final hour of trading on the third Friday of March, June, September, and December. It occurs when stock index futures, stock index options, and individual stock options expire. In the past this event was known to generate increased price volatility in the stock market due to an influx of orders needed to close existing positions or to initiate new ones on stocks that are price correlated with derivatives dealing within the expiration period. Whether triple witching still affects the market is a source of major debate today. Regulations also now limit certain types of short-term speculative trading activity which directly influences price correlations during these times. This means that triple witching hour may no longer represent a period of high price volatility for traders.

Trading Volatility can be a complex and potentially intimidating topic, but it doesn’t have to be. Essentially, it is the measurement of how quickly the price of an asset changes over time. Understanding the concept of volatility can provide insight into the potential risk and reward associated with different investments. For example, understanding that certain assets are more vulnerable to rapid swings in pricing over shorter periods of time allows savvy investors to make strategic decisions about where to invest their money. Similarly, by becoming familiar with stocks that exhibit consistent trends in pricing over longer periods of time, investors can gain an advantage in regards to both short-term and long-term returns. Finally, one can also capitalize on trading options contracts which allow a trader to benefit from price changes due to market volatility without actually owning the underlying asset in question. It’s clear that those who understand volatility have access to better opportunities than those who don’t.

Volatility in the stock market is often defined arithmetically as price correlations over a specified period of time. This refers to the degree to which price movements are statistically related, measured through price changes that rise and fall over a given length of time. Factors such as economic news, company earnings reports, or geopolitical events are some of the key drivers of price volatility in financial markets. When these events occur, they can have a major impact on price correlations and can cause dramatic price swings, adding more uncertainty in the stock market.

Volatility and risk are often used interchangeably. Volatility is the price change of a security over time and can be measured through price correlations and key drivers of price. Risk is the potential for losses from investing in a security; it involves both quantitative calculations such as volatility and qualitative decisions, such as a company’s credit ratings. Volatility and risk are often seen as synonymous when discussing the stock market, but they are not necessarily one in the same. Volatility describes how much an asset has the potential to fluctuate over time, while risk is the likelihood of permanent loss that comes with owning a particular asset or system. For example, many people tend to see stocks as inherently risky because there is always a possibility for permanent loss due to unexpected events or conditions. On the other hand, stocks may be volatile yet still have low long-term risk since there have been instances where stocks experience wild swings and then return to their original values over time. This highlights that understanding the difference between volatility and risk is important for investors when making decisions about which investments are right for them.

In the options market VOLATILITY specifically is the key determinant of options pricing. This is vital for traders and investors to understand who engages in strategies that involve stock index options, futures options or stock options contracts.

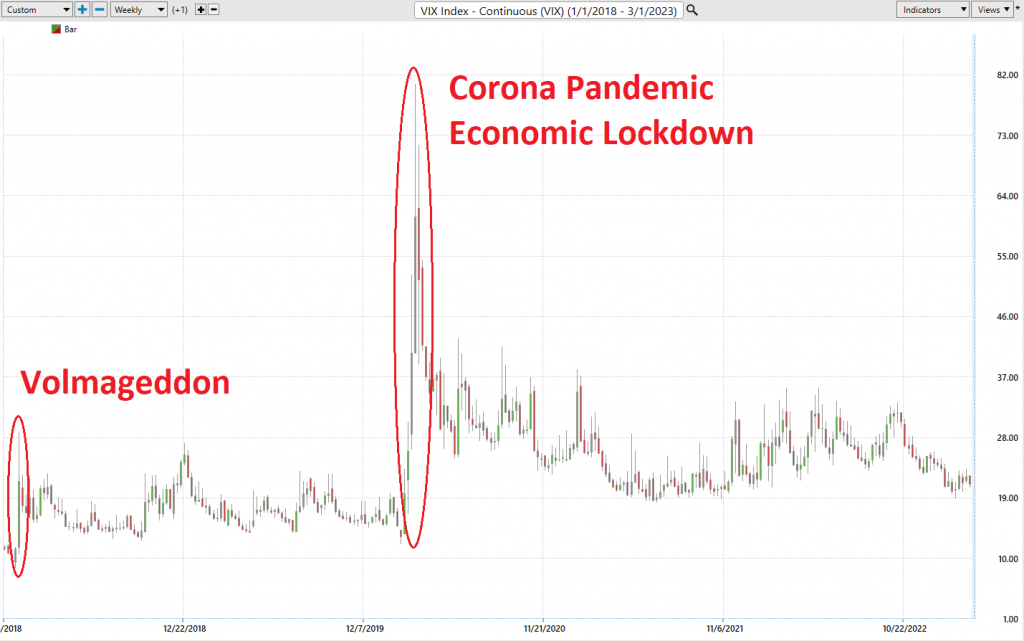

Below is a chart of the Volatility Index. When studying the Volatility Index ($VIX) in the stock market, there are some important rules of thumb for traders to understand. First and foremost, a down-trending VIX usually signifies a positive outlook on the direction of the overall market. Conversely, an up-trending VIX indicates either increasing levels of uncertainty or an expectation of increased volatility in the near future. The $VIX is determined by supply and demand levels for S&P 500 options, so stock traders should pay attention to shifts in these underlying markets as well. Ultimately understanding what moves the $VIX will enable more informed trading decisions which can result in higher profits over time. The sharp and sudden increase in the $VIX is a valuable and predictive indicator for traders to monitor.

.

When volatility spikes suddenly in the stock market traders recognize that risk is heightened. It is difficult to ascertain how long such conditions will last if it is simply just a blip on the radar. Traders have given these sudden spikes in volatility names which resemble end of the world scenarios. The most popular name is “Volmageddon.” Other contenders are “Volcalypse” and “Volacaust.” These names are attempts to describe real world conditions where RISK is severely heightened.

As an example, and historical reference on February 5, 2018, The CBOE Volatility Index increased by 100% in one day which caused massive losses for traders who were using options as risk management instruments. On a day like this, because of the huge spike in volatility option buyers did exceptionally well even if they were completely wrong in their direction of the market. This is because when volatility increases the price of TIME increases which is how risk is essentially defined. The term “Volmageddon” was coined after this occurred as numerous stock indexes ETF’s which were originally developed specifically to address volatility went out of business.

Market makers in the stock options market have issued numerous concerns about liquidity and risk during these sudden spikes in volatility. A market maker has the responsibility to provide liquidity in the options market. This means that they are prepared to buy and sell options contracts at any time to “make the market.” When market volatility spikes suddenly it is exceedingly difficult for market makers to define and effectively manage their risk. The result is much wider bid-ask spreads and/or reduced liquidity in the market. When liquidity concerns occur, it becomes more difficult for traders to execute trades thereby perpetuating the uncertainty and risk. Today many market makers are concerned about the risk associated with 0DTE’s which are Zero days to Expiration options. These options exist in the SPX and SPY every trading day. 0DTE’s are attractive to small speculators primarily because they are cheap, offer limited risk and unlimited reward potential.

Over the past several weeks these volatility risks and concerns have been brought to the attention of all market participants again as J.P. Morgan’s Mark Kolanovic who is Chief Global Market Strategist and Co-Head of Global Research warned traders of threats to stock market stability due to what he has referred to as “Volmageddon 2.0” risk in the options market. What Kalmanovich is referring to is that daily option expirations exist on the $SPY and $SPX and daily notional trading volume in these options is approaching $1 trillion dollars per day. $SPX and $SPY options have daily options expirations every Friday of every week, and every weekday for the upcoming two weeks. This is a perpetual schedule that has created tremendous liquidity in the options markets.

To understand what Kolanovic is referring to let’s do some simple options arithmetic based upon today’s $SPY expiring options.

There is an entire series of options that expire today March 2, 2023. To bring the concept of volatility centerstage let’s highlight exactly where the potential opportunity and risk reside.

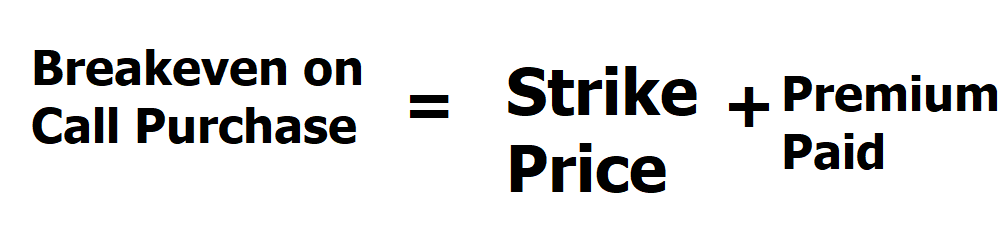

Whenever a buyer purchases a call option the most that he can lose is the premium that he pays for the option.

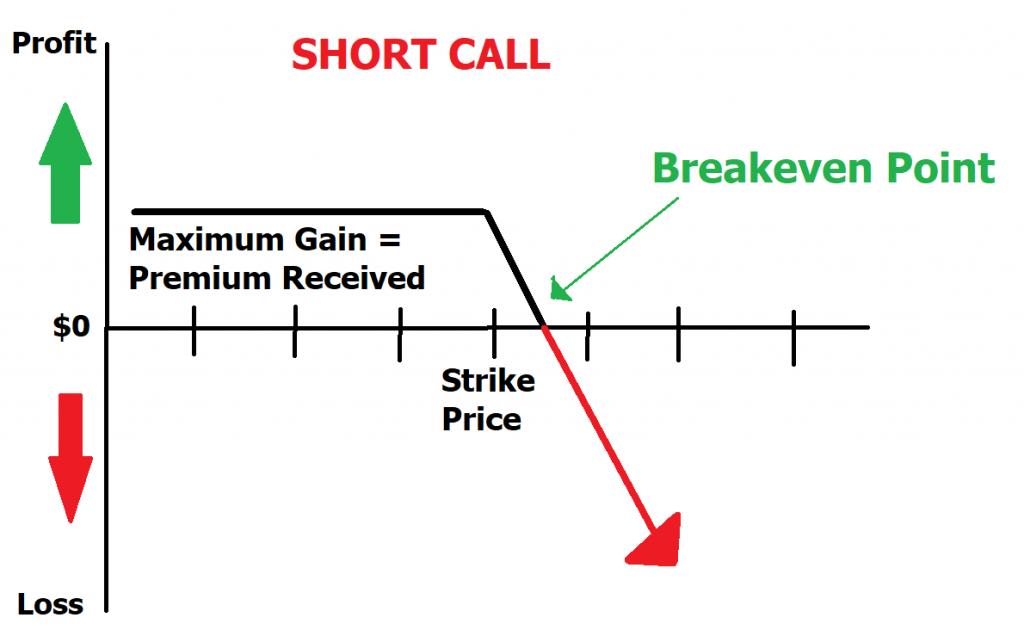

On the flip side whenever somebody sells an option, they are creating an obligation that they must be able to fulfill. The most that they can make is the premium they receive.

As I write these words $SPY is trading at $396.

Here are two call options which caught my attention and highlight the problem that Kolanovic is warning about. These options have only 4 hours left before they expire.

Strike Price Premium

399 .02

400 .01

If I purchase the March 2, 2023 $400 $SPY call option at .01 what I’m doing is risking $1 to have the right but not the obligation to purchase the $SPY at $400 between now and 4pm when the option officially expires. The chance of the option expiring worthless is very high. But as the option buyer my potential return completely depends upon where the $SPY is trading at 4pm this afternoon. If $SPY makes a 2% move to $403, my $400 SPY call option with a maximum risk of $1 would be worth $300.

The graph above represents what the risk-reward scenario looks like for the call option buyer. As a buyer, even though this is a low probability of success trade with my risk capped at $1 you can understand why many traders approach 0DTE (ZERO Days to Options Expiration) in this manner. Worst case scenario is the loss of $1.

But to understand the risk in this scenario let’s explore the market maker and their risk reward scenario. Whenever a trader sells a call option they create a contractual obligation. They collect premiums and in exchange they are obligating themselves to the terms of the contracts. In this case, the most that the seller of the call option can make is $1. The risk is theoretically unlimited because in theory the SPY INDEX could go to infinity. The risk/reward graph looks as follows:

The problem for market makers is that if they take this trade, they still have to manage it. The way most of them will manage it is they will place buy orders right at or below their breakeven price.

What JPMorgan’s Marko Kolanovic is saying is that the increasing popularity of 0DTEs has led to “a new form of Volmageddon,” which some have linked to the incredible volatility in February 2018. The bank’s research suggests that this volatility could have serious consequences for the broader market as it grows more prone to large intraday swings. When huge buy and sell orders congregate at certain price levels it is a recipe for Volmagedoon 2.0. These speculative bets can lead to excessive volatility in US markets and cause large swings in prices as they approach the final hour of trading at expiration. Since 0DTE’s happen every day this risk is ongoing for market makers. What is staggering to contemplate is that these 0DTE’s are creating $1 trillion in national trading volume every single day.

What many small speculators are doing is buying at the money calls and puts (straddles) a few hours before the options expires, anticipating a huge swing in one direction or another. While this is not a high probability trade should a large percentage of traders engage in this type of trade simultaneously it would be reminiscent of the panic that happened in GameStop ($GME)3 years ago when Wall Street Bets went up against large hedge funds who were massively short the market. As long as the market moves more than the premium paid the trade will generate a profit with limited risk.

For a market maker I can see how managing this type of risk is very problematic and would lead many market makers to not want to take the trade.

Here are some of the challenges that market makers face during 0DTE. All market makers are there to provide liquidity. Most of the time they are simply trying to take a market neutral stance while filling orders. The market makers recognize that if the underlying market stages a huge move in the last hour of trading that they have to unwind huge positions to try and stay market neutral. Here are the challenges they face trying to accomplish this objective.

- Difficulty Handling increased trading volume: The expiration of daily options contracts during 0DTE can lead to a surge in trading volume. Market makers need to be prepared to handle this increased volume to ensure that there is sufficient liquidity in the market.

- Managing market volatility: 0DTE can also be a time of increased market volatility as traders attempt to adjust their positions ahead of the contract expiration. Market makers need to be able to manage this volatility to prevent large price swings that could impact liquidity and disrupt the market.

- Ensuring fair pricing: As a market maker, it is important to ensure that prices are fair and reflect the supply and demand dynamics of the market. During 0DTE, large order flows can make it difficult to accurately price assets, leading to potential market distortions.

- Balancing risk and reward: Market makers need to balance the risk and reward of providing liquidity during 0DTE. On one hand, providing liquidity can be profitable, but on the other hand, it can also expose market makers to significant risk if they are not able to manage the increased volume and volatility.

- Meeting regulatory requirements: Market makers are subject to regulatory requirements that govern their activities, including requirements related to liquidity provision. During 0DTE, market makers need to ensure that they are complying with all applicable regulations while also meeting the demands of the market.

In conclusion, creating liquidity during 0DTE can be challenging for market makers due to the increased volume, volatility, and complexity of the market during this time. Market makers need to be prepared to manage these challenges to ensure that the market remains efficient, fair, and transparent. Otherwise, the 0DTE can create massive order imbalances that will create unprecedented market swings. Kolanovic believes these large price swings are baked into the macro picture and estimates it will result in moves up to $30 billion in intraday selling.

0DTE’s have gained huge popularity among money managers. In the past, market makers would refer to these expiring options as “learning to pick up nickels in front of an oncoming steamroller.” During the second half of 2022 0DTE’s consist of over 40% of the daily trading volume of the S&P 500 according to Goldman Sachs Research Group.

Options trading volume has exploded post pandemic.

Trading in options is concentrating on the shortest dated options.

50% of all traded options volumes are in options dated 5 days or less.

This is a market structure issue. Whenever you have excessive leverage in anything you can count on excessive risks occurring and things breaking.

These short, dated options are very attractive for options sellers because the time decay in the options is greatest in the final week before expiration. On the final day before expiration the decay is literally exponential.

In one regard what is occurring in 0DTE’s are low cost, highly leveraged, very calculated speculations. The inherent risk is that there is a cascading effect which can create flash crash type of moves if these volumes continue to grow as they have in 2022.

0DTE’s create order flow. Be forewarned.

If you are attracted to 0DTE’s it’s important to understand this concept by practicing in a demo account and you will quickly come to understand the risks and possibilities.

In a demo account you will quickly come to understand that leverage is always a two-edged sword. You will quickly come to understand potential rewards and real-world risks in 0DTE’s. There is an encyclopedias worth of education to learning about options which become void the same day they are traded.

What’s Your Best Chance to Make Money in The Financial Markets Today?

The Answer A.I. offers will surprise you.

Today Artificial Intelligence, Machine Learning and Neural Networks are an absolute necessity in protecting your portfolio. Imagine if you received a forecast that was up to 87.4% accurate about the direction of an underlying stock or Index 3 to 5 days in advance. Would that be valuable to you?

The job of A.I. is to find those stocks with the best trends, either Up or Down, and highlight where the risk lies in that market.

Bad Traders Obsess over the SHOULD. Every other word out of their mouths’ is SHOULD.

I can’t recall how many times a trader has told me all the reasons why his portfolio is heavily invested in a stock because of a great story, despite the stock being in a firm downtrend.

But when “SHOULD” and “IS” meet some pretty explosive things can happen. And that is exactly where we want to be as traders!

Great trading is never about how much you make when you are right. It’s always about how little you lose when you are wrong.

Artificial intelligence is so powerful because it learns what doesn’t work, remembers it, and then focuses on other paths to find a solution.

Artificial Intelligence applies the mistake prevention as a continual process 24 hours a day, 365 days a year towards whatever problem it is looking to solve.

Be beautifully positioned before the herd even knows what happened.

Manage the RISK on the trade.

Lather. Rinse. Repeat.

The Answer AI offers may surprise you.

This is how some small traders grow their accounts by taking small bites out of the market consistently.

Today Artificial Intelligence, Machine Learning and Neural Networks are an absolute necessity in protecting your portfolio.

Intrigued? Visit with us and check out the a.i. at our Next Live Training.

Discover why artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

It’s not magic. It’s machine learning.

Make it count.

IMPORTANT NOTICE!

THERE IS SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.