What is your edge in trading? That is a very simple question and how you answer it will often dictate your long-term performance.

Markets can be extremely volatile and at times difficult to trade. These moments often open a trader up to recognizing that there are numerous ways to profit from volatility. However, to really create an edge it is essential that a trader understand the risks, rewards, and realities of options trading.

Exchange-traded options are financial contracts that give the holder the right, but not the obligation, to buy or sell an underlying asset at a set price on or before a specified date. Options are traded on exchanges such as the New York Stock Exchange and Chicago Board Options Exchange, and they can be used to speculate on the future direction of the markets or to hedge against downside risk. There are two types of options: call options and put options. Call options give the holder the right to purchase an asset, while put options give the holder the right to sell an asset.

Options are the most popular and effective way that traders manage risk. But what is critical to understand is while options act as INSURANCE they also are deteriorating assets. Because options contracts have a limited lifespan, they are classified as deteriorating assets. As the expiration date approaches, the options contract loses value at an accelerated rate. This is due to the time decay of the option, which is affected by factors such as the volatility of the underlying asset and the amount of time left until expiration. One of the most effective ways that Power Traders capture Time Decay is using the Calendar Spread.

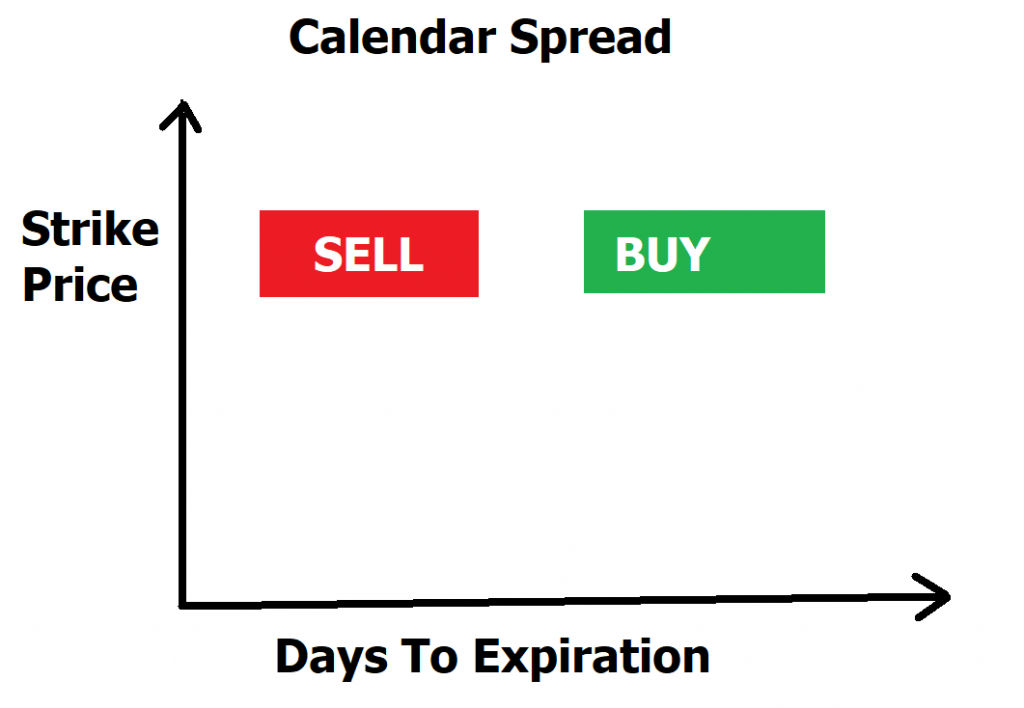

A calendar spread, also known as a horizontal spread, is created by buying and selling options with different expiration dates but the same strike price. The options are bought and sold at the same time. This strategy has a neutral directional bias, and as long as the market trades in and around the strike price the trade will be profitable because the time decay will occur faster in the front month than in the back month.

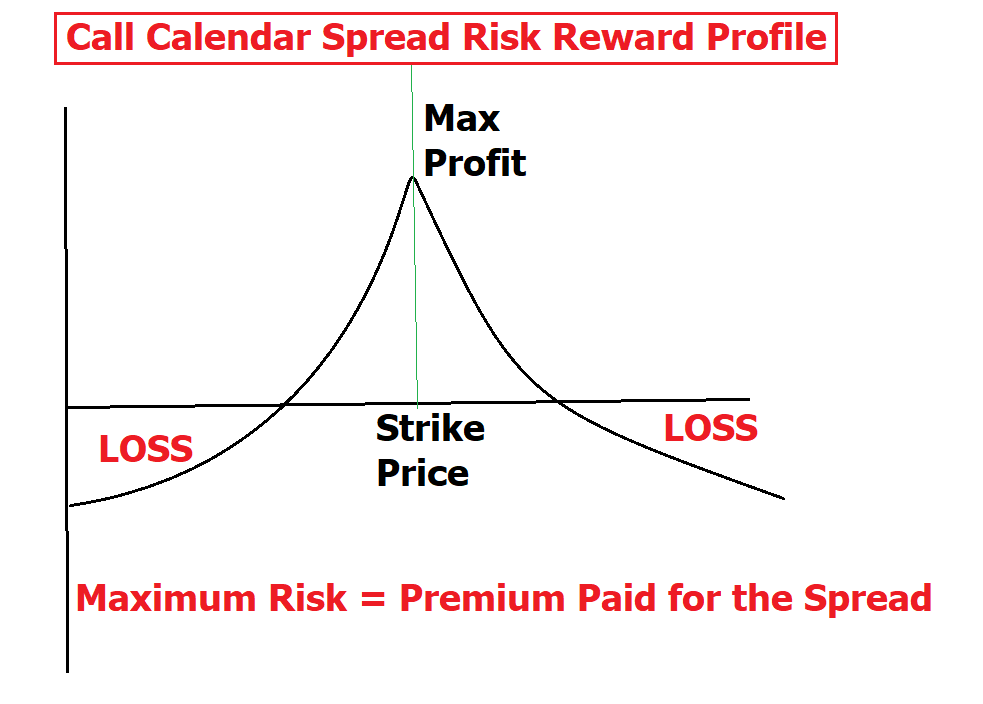

The most effective means of visualizing this trade is through the following graphic described visually.

The front month option is sold and the exact same strike price on a back month option is bought. The number of options purchased is equal to the number of options sold. In other words, the entire purpose of the trade is to capture time decay at an accelerated pace and protect your risk should a massive rally occur. This is referred to as a calendar spread and it consists of selling the front month options series and buying a back month of the same strike price.

At first glance the strategy can seem counterproductive if a trader does not understand the nuances and subtleties of time decay.

When you buy an options contract, it gives you the right to buy or sell a certain asset at a set price. This contract has a time limit, called the expiration date. When the expiration date arrives, the contract expires and is no longer valid. Until that exact date, the contract will lose value gradually over time. This is called time decay. The longer the expiration date is, the more time there is for the underlying asset to move in the direction you want, so the value of the contract is greater and will decrease at a lesser pace than an options contract with less time till its expiration date. The closer it gets to the expiration date, the faster the value of the contract decays.

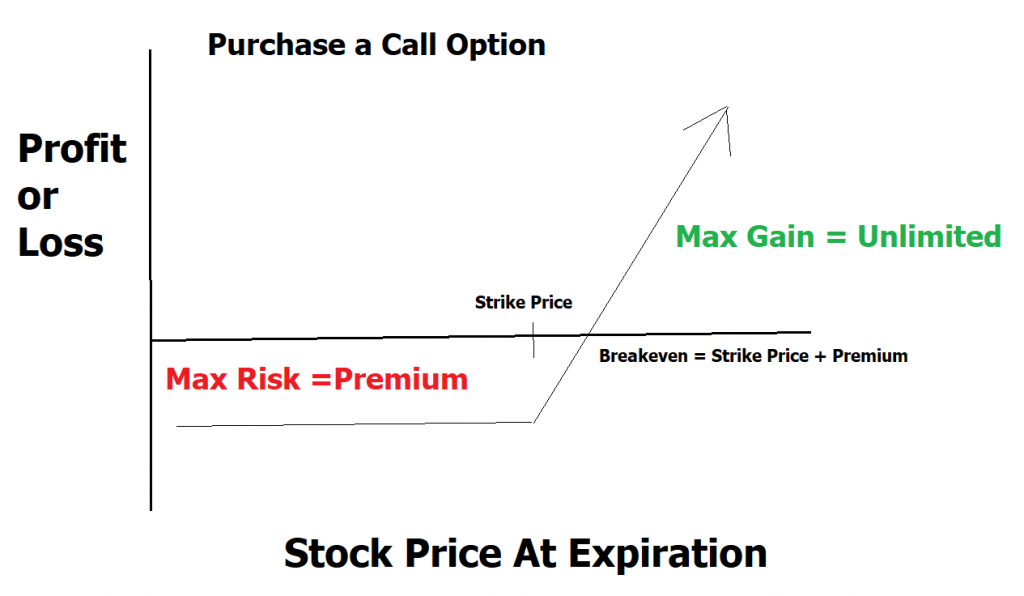

Here is the risk/reward profile of purchasing a call option.

The most that an options buyer can lose is the premium they paid for the option. Theoretically, the most they can make is theoretically unlimited because the stock price could go to infinity. The reality is that 70% to 80% of all options expire worthless. So, the buyer of this option must have the stock move to above the strike price, plus then add the premium they paid for the option to calculate their break-even price at expiration.

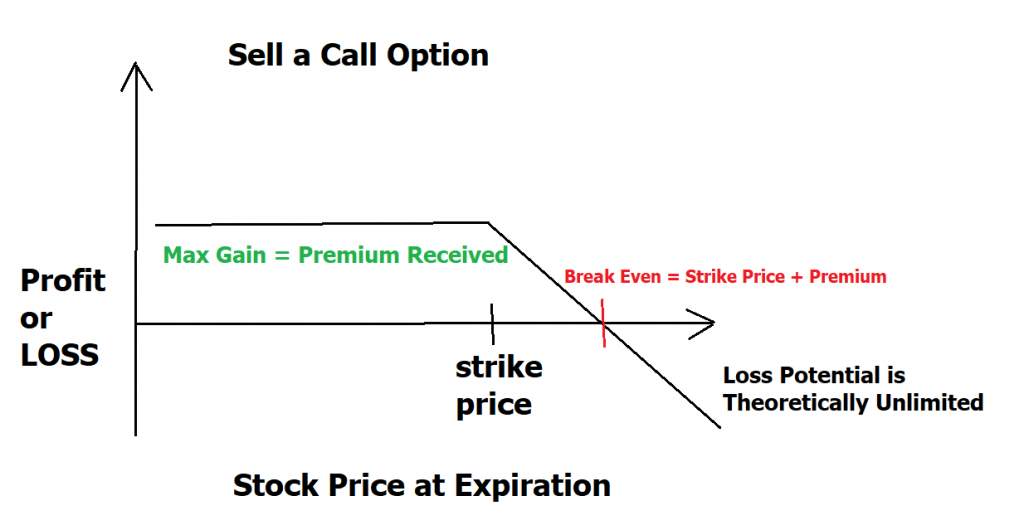

On the flip side, a call option seller is creating an obligation. They are accepting a premium payment and agreeing that they will deliver the underlying asset at the agreed upon price at expiration. The most amount of money they can make is the premium they collect. Their risk is theoretically unlimited because the stock can go to infinity. Here is the risk/reward profile for a naked call option seller:

By combing both strategies, selling a call option in a front month, and buying a call option in a back month a Power Trader is creating a risk managed position where they are capturing time decay and giving themselves a mathematical edge in their trading.

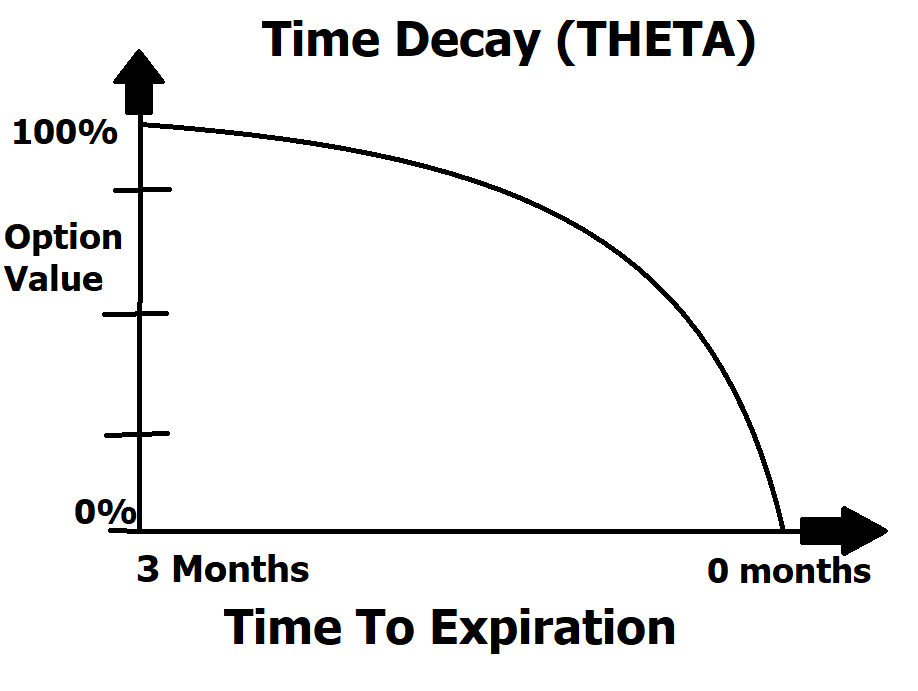

The most effective way to illustrate this idea is through the following graphic. You can quickly see that in the last 30 days of an options life its decay is exponential. The calendar spread options strategy is designed specifically to take advantage of this reality. It does this by specifically selling premium in the nearby month and buying premium at the same stroke price in the distant month.

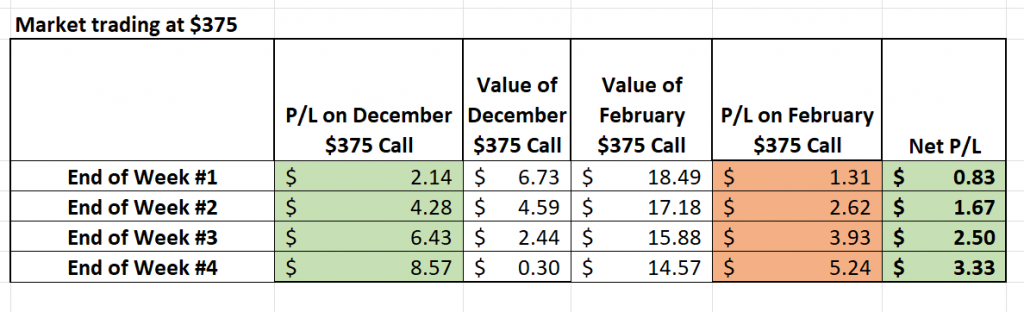

For example, let’s look at the SPDR S&P 500 SPY Index options.

The market is currently trading around $375.

The 375 call options expiring on December 2, 2022, are trading at $8.87.

There are only 29 days left till expiration.

So, we can divide the total premium of $887 and divide it by 29 days and calculate that all things being equal this option will decay in value at a pace of roughly $30.60 per day.

The February 17, 2023, $375 strike price call options they are trading at $19.80. They have 106 days left before they expire.

When we divide the total premium of $1,980 by 106 days, we can calculate that the option will decay at a rate of $18.70 per day.

The difference between the two-time premiums decay is the profit of loss.

So, we are capturing time decay of $30.60 per day.

And we are losing time decay of 18.70 per day.

The difference is a positive $11.90 per day.

Your goal as a trader is for time decay to work in your favor. All else being equal, an option will lose value as it gets closer to expiring. As long as the price action stays around the $375 strike price over the next 29 days, this strategy will be a winner.

Another simple way of thinking about this is that in essence you are shorting TIME.

Short 1 call option with 29 days left till expiration

Buy 1 Call option with 106 days left till expiration

Net cost = Maximum Risk

As a general rule, nearer-dated options will experience more time decay than longer-dated options. That’s why selling the front-month option and buying back the following month’s option generally benefits Calendar Spread traders. The front month option decays 2.5% faster than the back month in this instance which is a powerful edge in stable market conditions.

The maximum profit occurs if the stock price equals the strike price of the calls on the expiration date of the short call. As expiration of that front option approaches, a decision needs to be made. Your short call will soon expire, and if you do nothing before expiration, you could be left with half a spread.

If the market is trading at the strike price that is the point of the maximum profit, because the long call still has time value remaining when the front month call expires. the stock price equals the strike price. Also, since the short call expires worthless when the stock price equals the strike price at expiration, the difference in price between the two calls is at its greatest.

It is not possible to know for sure what the maximum profit will be, because the maximum profit depends on the price of a long call which can vary based on the level of volatility when the short call expires.

These option legs do not have to be held till expiration. They can be closed out at any time. The objective is to try and capture as much of the time decay as possible in the front month as long as the underlying market continues trading at or near the strike price.

If the stock price moves too far in either direction, your trade could experience losses. Too far in this regard, as a rule of thumb is roughly equivalent to the net premium paid for the spread. The maximum risk of a long calendar spread with calls is the cost of the spread. If the stock price moves sharply away from the strike price, then the difference between the two calls approaches a value of zero and the full amount paid for the spread is lost. So, if the stock price falls sharply, then the price of both calls approach zero. If the stock price rallies sharply then both calls are deep in the money, and the prices of both calls approach parity for a net difference of zero.

Here is what the profit and loss on this trade looks like 4 weeks out with an estimated profit and loss analysis at the end of each week, as long as the market remains in the vicinity of the $375 strike price.

Sell 1 29 day $SPY $375 Call Option at $8.87

Buy 1 106 day $SPY $375 Call Option at $19.80

That’s why it’s important to only use this strategy when you have a clear idea of where the stock might be headed and you’re comfortable with the potential risks involved. When done correctly, though, Calendar Spreads can be a great way to take advantage of expected time decay.

It’s all about choice. The more choices you have in trading the more powerful of a position you have and that is why I behoove you to study Options trading very carefully. It could pay dividends because you can enter strategies that are directionless and still profit, but nothing is guaranteed.

Whenever you trade a stock, the relationship between profit and loss is very black, white, and linear. But when you trade options the opportunity to put odds overwhelmingly in your favor exists because of aspects like time decay.

There are five potential outcomes in any trade:

- You make money if the stock goes up a lot

- You make money if the stock goes up a little

- You make money if the stock remains unchanged

- You make money if the stock goes down a little

- You make money if the stock goes down a lot

A skilled options traders can create a risk reward profile that benefits from most of the above possibilities on each trade they take. This is what makes options trading so exciting. Therefore creating strategies which exploit time decay are worth your further study. This is how Power Traders create their EDGE.

You can read our Options Primers here:

What makes this tactic worthy of your time and study is that options expirations currently are occurring on $SPY options every day of the week which means that this tactic can be applied on a very granular level. Options have been trading actively for about 50 years, but only in the past several weeks have we seen a large demand for weekly options expirations as well as daily options expirations.

What’s Your Best Chance to Make Money in The Financial Markets Today?

The Answer A.I. offers will surprise you.

Today Artificial Intelligence, Machine Learning and Neural Networks are an absolute necessity in protecting your portfolio. Imagine if you received a forecast that was up to 87.4% accurate about the direction of an underlying stock or Index 1 to 3 days in advance. Would that be valuable to you?

The job of A.I. is to find those stocks with the best trends, either Up or Down and highlight where the risk lies in that market.

Bad Traders Obsess on the SHOULD. Every other word out of their mouths’ is SHOULD.

I can’t recall how many times a trader has told me all the reasons why his portfolio is heavily invested in a stock because of a great story, despite the stock being in a firm downtrend.

But when “SHOULD” and “IS” meet some explosive things can happen. And that is exactly where we want to be as traders!

Great trading is never about how much you make when you are right. It’s always about how little you lose when you are wrong. When you learn how to sell Options and collect premiums you can be wrong and you could still make money.

Artificial intelligence is so powerful because it learns what doesn’t work, remembers it, and then focuses on other paths to find a solution.

Artificial Intelligence applies mistake prevention as a continual process 24 hours a day, 365 days a year towards whatever problem it is looking to solve.

You can learn to sell risk managed Options with minimal risk exposure and sound money management.

Be beautifully positioned before the herd even knows what happened.

Manage the RISK on the trade.

Lather. Rinse. Repeat.

The Answer AI offers may surprise you.

This is how some small traders grow their accounts by taking small bites out of the market consistently.

Today Artificial Intelligence, Machine Learning and Neural Networks are an absolute necessity in protecting your portfolio.

Intrigued? Visit with us and check out the a.i. at our Next Live Training.

Discover why artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

It’s not magic. It’s machine learning.

Make it count.

IMPORTANT NOTICE!

THERE IS SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.