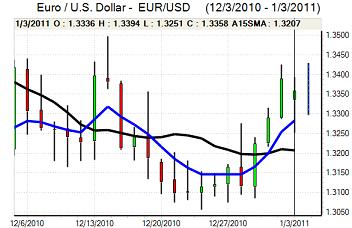

EUR/USD

Market liquidity remained very low in the run-up to the New-Year holiday weekend and there was a spike in currency volatility with the Euro advancing sharply to highs just above 1.3410 against the dollar on Friday with some last-minute position adjustment.

As far as US economic releases are concerned, the pattern has remained favourable over the past few days and confidence in near-term growth prospects has increased. Jobless claims dipped to below the 400,000 level for the first time in over two years while pending-home sales also increased. In the manufacturing sector, there was an improvement in the PMI index to a seven-month high of 57.0 for December from 56.6 the previous month.

Evidence of a firmer economy will tend to boost the dollar on hopes for investment inflows and there will also be speculation that the Federal Reserve may look to adjust its quantitative easing programme during the first half of 2011. There will be a mixed impact on the dollar as there will also be a general improvement in risk appetite which will increase the potential for carry trades funded through the dollar.

The Euro-zone debt developments will continue to be an extremely important market focus and there will be further concerns that funding pressures will increase quickly in the first quarter of 2011. There has also been evidence of Euro-zone bond redemptions which will maintain the potential for Euro selling. The currency was unable to hold above 1.34 and weakened to test support below 1.3350.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

Yen

The dollar remained under pressure against the yen at the end of last week and tested support just below 81 with evidence of last-minute capital repatriation. The weight of capital flows more than offset the impact of positive US economic news.

The dollar was able to regain ground once the new-year started with a move to the 82.10 area. The US currency gained support from an increase in US Treasury yields and the impact of capital repatriation also faded. There will still be underlying fears over the Euro-zone capital markets which will tend to stem capital outflows from the Japanese currency.

Overall confidence in the Japanese economy remains weak and there have also been renewed stresses surrounding the government which will tend to unsettle the Japanese currency to some extent. There will be strong pressure on the Japanese authorities to resist yen appreciation.

Sterling

Sterling volatility spiked higher ahead of the weekend with low trading volumes exaggerating the impact. After testing lows below 1.5350 against the dollar, the UK currency pushed sharply higher to a peak above 1.5650 as the US currency was generally weaker.

There were last-minute capital flows which helped underpin Sterling, but there were also fundamental doubts surrounding the UK economy.

The Nationwide house-price index was stronger than expected with a 0.4% monthly increase for December following a 0.3% decline the previous month, but housing-market liquidity is very low at this time of the year and underlying confidence in the sector remains weak.

There will also be expectations of a wider deterioration in the economy as tax increases take effect and this will tend to undermine confidence in Sterling with a move back to below the 1.55 level against the US currency as 2011 trading got under way.

Swiss franc

The Swiss franc maintained a very firm tone on the crosses ahead of the year-end with the franc testing record levels against the US dollar and Euro with the US currency dipping to a trough just below 0.93 before finding some degree of support.

Domestically, the Swiss PMI index fell to 59.6 for December from 61.8 the previous month. Although the index is still high in relative terms, there will be further speculation that the economy is being undermined by a strong franc.

Although year-end flows eased, the Swiss currency maintained a strong tone at the beginning of 2011 which will maintain speculation that there are still very important defensive inflows into the franc.

Source: VantagePoint Intermarket Analysis Software

Call now and you will be provided with FREE recent forecasts

that are up to 86% accurate * 800-732-5407

If you would rather have the recent forecasts sent to you, please go here

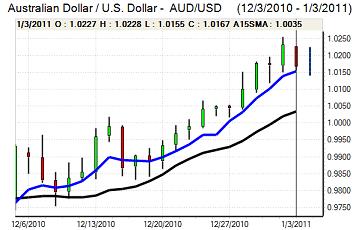

Australian dollar

The Australian dollar maintained a very firm tone at the end of last week and pushed to fresh 28-year highs above 1.0220 against the US dollar.

Commodity prices remained very strong which helped underpin the Australian dollar and there was further near-term optimism surrounding the global economy. The Chinese PMI data was slightly weaker than expected which dampened the Australian dollar and there were some concerns over potential export damage from flooding which could have an impact on Reserve Bank interest rate policy.

A reversal of year-end flows was the principal factor and the currency retreated back to below 1.01 in Asian trading on Tuesday.