I’m a Chartaholic.

I love looking at charts. I’m addicted to trying to best understand what makes charts behave the way they do.

Sometimes charts don’t have anything to say. But sometimes they tell a story that others have yet to discover.

Over the last several months I’ve been studying the currency charts of different countries and reading analysts opinions about why the currencies are behaving the way that they are.

Traditional fundamental analysis can be rather abstract. In the past traders were always conditioned to believe that when a currency became strong relative to another currency pair, it was a sign that one economy was usually stronger than the other.

In December 1996, then-Federal Reserve Chairman Alan Greenspan made a now-infamous remark about “irrational exuberance” in the stock market. But what did he mean? And what implications does it have for today’s investors?

Here is what Mr. Greenspan said and he was frank about the knowledge problem facing central bankers:

“[There is no] bound volume of immutable instructions on my desk on how effectively to implement policy to achieve our goals of maximum employment, sustainable economic growth, and price stability. Instead, we have to deal with a dynamic, continuously evolving economy.… There is, regrettably, no simple model of the American economy that can effectively explain the levels of output, employment, and inflation. In principle, there may be some unbelievably complex set of equations that does that. But we have not been able to find them.

I doubt the tasks will become any easier for the Federal Reserve as we move into the twenty-first century The Congress willing, we will remain as the guardian of the purchasing power of the dollar. But one factor that will continue to complicate that task is the increasing difficulty of pinning down the notion of what constitutes a stable general price level.”

To understand Greenspan’s comment, it’s first important to understand what money is and how it is created. Money is simply a unit of account that we use to measure value. When we talk about the “money supply,” what we’re really talking about is the total amount of money in circulation. This includes cash and cash equivalents, like savings accounts and short-term government bonds. It also includes more liquid assets, like checking accounts and money market funds. Finally, it includes less liquid assets, like long-term government bonds and stocks. To understand what Greenspan was getting at, it’s important to first understand what money is. Money is simply a means of exchange – it’s useful because we can use it to buy goods and services. But what gives money its value? In a word: valuation. The value of money is based on what people are willing to trade for it.

So, what does that have to do with irrational exuberance? Well, in the late 1990s, there was a lot of excitement around the stock market. People were investing heavily based upon the excitement that the internet was bringing to tech stocks, and prices were soaring. But Greenspan was worried that this wasn’t based on any real fundamentals – in other words, people were trading based on hype rather than actual value. Greenspan was also saying something else in that historic speech which every investor and trader should pay greater attention to. Greenspan was admitting that it was becoming harder and harder to define what money is.

My interpretation of this speech is that Mr. Greenspan was admitting that it was becoming more, and more difficult to define money, its relationship to a healthy economy and the purchasing power of your dollars. The Federal Reserve is armed with thousands of statisticians who build econometric models to uncover relationships between all aspects of economic activity. Yet, in spite of this quantitative battalion of economists, Greenspan was admitting that as a central planner he was unsure and unable on how to navigate the monetary maze effectively.

Everyone remembers the phrase “irrational exuberance” from Greenspan’s speech, but the majority have never listened to or read the entirety of the presentation which can be found on the Feds website. At that time, the NASDAQ was trading around 1,300. By the time the dotcom bubble had burst in 2000, the NASDAQ had reached 5,000 – a gain of nearly 300%.

The market then experienced a dramatic decline, culminating in the NASDAQ tech market implosion of 2001 before plunging all the way down to 1,114 in October 2002.

I’ve been thinking about Mr. Greenspan recently as I’ve been watching the Eurodollar market for the last year. Most people have a distant familiarity with the Eurodollar market, but its infrastructure and internal plumbing remain a mystery to even seasoned experts and veterans.

Eurodollars are U.S. dollar-denominated deposits held in foreign banks. The term “Eurodollar” originally referred to U.S. dollars deposited in European banks, but the term is now used to refer to any U.S. dollar-denominated deposit held outside the United States. Eurodollars are often used for international transactions and to avoid regulation by the Federal Reserve.

The history of Eurodollars dates to the early 1950s, when American companies began setting up branches in Europe to take advantage of the lower interest rates there. In response, the Federal Reserve began imposing restrictive regulations on these companies’ activities, which led them to begin depositing their dollars in foreign banks instead. The Eurodollar market really took off in the 1970s, when high inflation and interest rates in the United States made foreign banks an attractive option for savers and investors.

Since Eurodollars are U.S. dollars deposited in banks outside the United States, they are not subject to reserve requirements or other regulations of the Federal Reserve System. For example, a French company may have business operations in the United States and need to maintain a dollar-denominated account for its American customers, but it would deposit those funds in a Paris bank to avoid American reserve requirements. Today, Eurodollar deposits are used extensively in international lending and borrowing between banks and other financial institutions. They are also commonly used by multinational corporations for their own financing needs. Thus, the main purpose of Eurodollar transactions is to avoid regulation and reserve requirements by using banks outside the United States.

Today, Eurodollars are still widely used for international transactions and to avoid regulation by the Federal Reserve but to also transact with the U.S. dollar as the worlds reserve currency. However, the Eurodollar market does not have any regulatory authority overseeing it and more importantly regulators cannot determine how large it is. The size of the Eurodollar market is difficult to estimate because it is an unregulated market and data is not centrally reported or published. Nevertheless, some experts believe that the Eurodollar market to be equivalent in size to the Treasury market.

In the past, the way Eurodollars were explained is they would increase in value when the demand for dollars was strong. Likewise, they would decrease in value when the demand for dollars was weak This concept always made sense and allowed me to ascertain the strength, or the weakness of the U.S. economy based upon the health of the Eurodollar market… Until now.

In the graphic above you see the last 9 months of price action in the Eurodollar market. I have labeled the three significant fundamental events which I think confirm that de-dollarization is occurring.

Let me explain.

In November of 2021, the Fed started discussing the possibility of raising interest rates and tapering their purchases of Treasuries. Then on February 24, 2022, Russia invaded Ukraine and a few days later the United States and Europe imposed economic sanction on Russia and seized Russian assets. Lastly, on June 23, 2022 Mr. Putin and the BRICS nations releases a new declaration regarding international trade away from the U.S. dollar with the XIV Summit Beijing Declaration.

As a chartaholic, I’m simply offering my opinion on what is occurring in the world right now based upon some charts that have caught my attention. But trying to make sense of these charts paints a story I don’t hear many in the financial media discussing. The world is awash in FIAT debt, and no one wants it.

We are witnessing the birth of a new monetary order centered around hard currency and commodity-based assets. These currencies are a direct threat to the Eurodollar system and the inflationary policies engaged in by monetary authorities in the West. Mr. Greenspan in his infamous “irrational exuberance” speech warned that in 1996 it was becoming increasingly difficult to define money and thus it was not possible to determine rational expectations. Today, Mr. Putin is challenging the democracies of the West and forcing them to recognize that Commodities and real assets serve as much better collateral than FIAT.

Western financial sanctions against Russia in response to the war in Ukraine appear to have done more damage to the West than to their intended target. Freezing another countries FX reserves appears to have frightened and intimidated other counterparties from initiating in dollar denominated trade.

Stop and think for a moment that your bank account was frozen any reason. How much trust would you have in the bank moving forward? Would you recommend the bank to others?

Well, the world has been watching Western democracies effectively freeze Putin’s assets. Regardless, of whether you agree or disagree with such measures, other countries are concluding that holding U.S. dollar denominated assets has the additional risk of forfeiture should you disagree with political policies. Western sanctions are simply driving Russia and China into a tighter partnership further and further away from financing U.S. deficits with their purchase of Treasuries.

Saudi Arabia is already discussing changing their purchases of Oil from the U.S. Dollar to the Chinese Yuan. After all what is the appeal to purchase U.S. Treasuries which offer negative real yields? If the U.S. will seize Russian assets, might they seize Saudi assets as well?

At present these questions are scaring market participants. But what is clear is that there has been a clear exodus out of Eurodollars. Since Eurodollars represent American hegemony and debt this is noteworthy.

Let’s look at a few charts and I’ll share my opinion of why this fundamental de-dollarization theme is the primary force to be reckoned with in the financial markets at the present time.

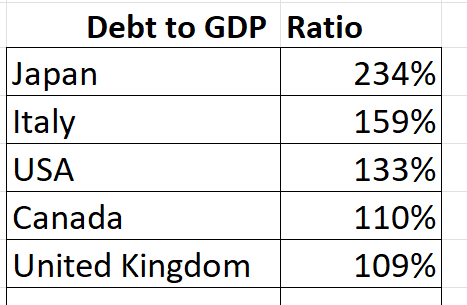

First off, let’s look at the Debt to GDP ratios of some of the largest nations in the world.

Now let’s look at how some of these currencies have performed. Japan is the most indebted nation in the world with a debt to GDP ratio of 234%.

Let’s look at the Euro which is currency of Europe. Over the last year the EURO is down 14.24%. It is also 93.6% correlated to the Eurodollar. So, it appears that markets are rejecting indebtedness as well as the last 8 years of ZERO interest rate policies of the European Central Bank.

The British Pound chart looks almost identical to the Euro.

My conclusion that these massive selloffs are nothing more than these countries debasing their currencies. The race to debase is very real.

But this is where it gets interesting. Look at the following chart of the Russian Ruble versus the U.S. Dollar.

The Russian Ruble has risen 44% since Russia invaded Ukraine.

The Bretton Woods system, established in 1944, pegged the value of the US dollar to gold and made it the world reserve currency. Other currencies were pegged to the dollar, making it the key currency in global trade. However, this system began to unravel in the early 1970s as inflationary pressures forced the US to abandon the gold standard. Since then, the dollar has remained dominant due to a variety of factors, including the size of the US economy and the stability of its political and financial institutions. However, there are now signs that this hegemony is coming to an end. A growing number of countries are pursuing de-dollarization, which refers to a shift away from using the dollar in international trade and investment. The implications of de-dollarization are significant. As more countries adopt this approach, it will lead to a decline in demand for dollars, but since it is the reserve currency of the world, in theory it could still increase in value as other currencies race to debase faster than the greenback. This could have major implications for the global economy, which has become increasingly reliant on the dollar over time.

At the present moment, this is what de-dollarization looks like.

Fiat currencies are debasing as fast as possible. Many countries are reducing their reliance on the US dollar, either by switching to another currency or by pricing international trade in their own currency.

There are several ways to measure de-dollarization, but one common approach is to track the share of international trade that is priced in foreign currency. If this share is begins increasing, it suggests that de-dollarization is occurring. Another way to measure de-dollarization is to look at the share of central bank reserves held in US dollars. Currently, 61% of all world trade occurs in U.S. dollars. This share is expected to decline as Brazil, Russia, India, China, South Africa, and several other nations diversify their holdings away from dollars. Finally, we can also look at the share of global debt issued in US dollars. If this share starts falling, it suggests that borrowers are increasingly turning to other currencies. Together, these various indicators provide a clear understanding of de-dollarization trends.

But the bottom line really is how does all of this affect you and your portfolio?

The U.S. dollar has been king of the hill for almost 80 years. What many politicians and journalists do not understand is that the sun is setting on U.S. global leadership. While freezing Russian assets garnered headlines the long-term consequences of expropriating another nation’s assets have accelerated the trend toward a new monetary order. Trust in the West is evaporating. We will be watching and reporting on these trends moving forward.

These events are challenging the way the world defines money.

As a trader, I would urge you to pay close attention to this discussion.

How do great traders define risk? It’s a question that has puzzled novices for years. After all, if the defining risk were easy, everyone would be a successful trader. The truth is, there is no single answer to this question. Different traders have different approaches, and what works for one person may not work for another.

However, the common theme of using artificial intelligence to isolate opportunities is what traders today should embrace to minimize risk as much as possible.

We are in uncharted waters.

Traditional economic theories don’t work for traders.

The only thing that a trader is concerned with is being on the right side, of the right market at the right time.

And that means harnessing the power of VantagePoint’s artificial intelligence.

Everything else is just noise.

The race to debase is very real. This economic environment is forcing traders into much shorter time frames as everyone in the marketplace chases yield.

Real asset prices will keep rising as the yield chase intensifies. Cheap capital will keep flooding the market. And our economy will continue its addiction to a horrible monetary stimulus.

Do you have the tools and ability to find the strongest trends at right time in this economic environment?

What is your plan for maintaining your purchasing power as this trend accelerates?

I’d like to invite you to visit with us at one of our live Master Class Webinars where we show how artificial intelligence is the only means to stay consistently up to date on the risk and reward opportunities in this environment.

What all traders and investors want is an accurate, proven solution that alerts you when a high probability trend is unfolding. The Vantagepoint A.I. forecasts have proven to be up to 87.4% accurate in determining the trend three days in advance.

Visit with us and check out the A.I. at our Next Live Training.

It’s not magic. It’s machine learning.

Make it count.

IMPORTANT NOTICE!

THERE IS SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.