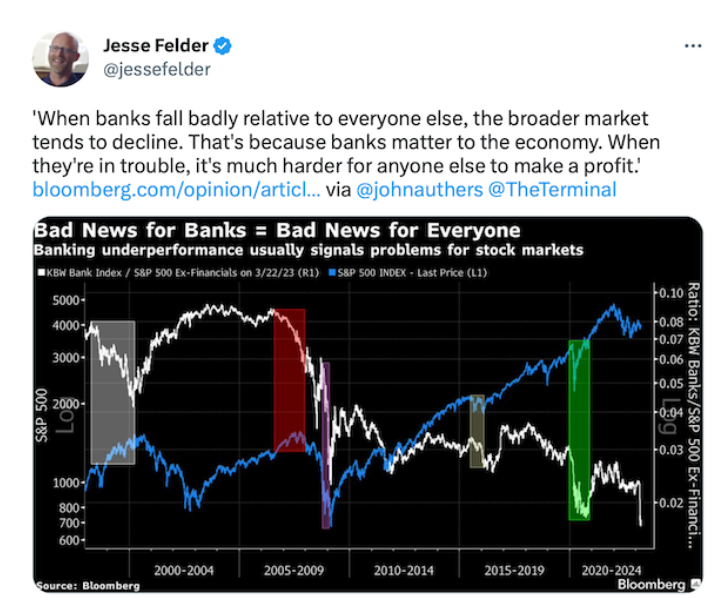

One of the things I do every week in preparation to write this blog is study charts, read financial journalists, and peruse social media to try and get my finger on the pulse of what people and traders are focused on. Since the banking crisis began, I’ve been troubled by how quickly it’s been swept under the rug to create an appearance of normalcy.

The great fiat experiment began 52 years ago on August 15, 1971 when President Nixon took the nation off the gold standard. We now have over 5 decades of persistent currency debasement. How much more evidence is necessary before we return to a sound monetary system? The printing press allows the government to throw money at every problem as a “fix.” But I’d argue the prevailing issue with today’s economy stems from the government’s tendency to address challenges by simply injecting vast sums of money into them, in the hope of achieving quick solutions. While this strategy may appear to offer temporary relief, it often leads to long-term consequences such as increased inflation, mounting debt, and unsustainable economic growth. Furthermore, this approach does little to address the root causes of the problems at hand, instead merely providing a short-lived boost that may exacerbate existing issues. The long-term health of the economy would be better served by a more strategic and targeted approach, focusing on addressing systemic issues, promoting sustainable growth, and fostering innovation rather than relying on the blunt instrument of excessive fiscal spending.

Thirty-one years ago, James Carville was the lead strategist for Presidential candidate Bill Clinton. One of Carville’s most memorable remarks occurred when he said: “I used to think that if there was reincarnation, I wanted to come back as the president, or the pope, or as a .400 baseball hitter. But now, I would like to come back as the bond market. You can intimidate everybody!”

The Bond market is the largest market in the world. Its behavior over the last 18 months is worth paying attention to because it has all of the earmarks of a vicious debt spiral. It’s a toxic mix of ballooning borrowing costs, a crumbling fiscal position, and evaporating confidence from creditors. Put simply, it’s a recipe for disaster, leading to a sovereign debt crisis that sends shockwaves through the economy. I’ve written about this in previous blog articles which you can find here.

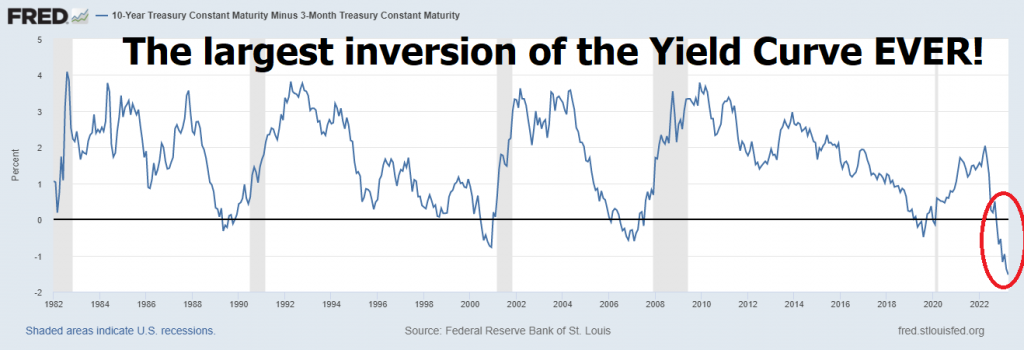

The real problem for traders, as well as policymakers, is that the 3 months versus 10 year spread on the yield curve is at its worst position in history. This is an indicator that has never sent a false signal about the prospects for a recession in over 50 years!

When short-term bonds have higher yields than long-term bonds, that’s called an inversion, and it’s a clear sign of trouble ahead.

This is the most deeply inverted gauge in the bond market history, and it is pointing to a major economic slowdown. And while some analysts are still hopeful that this could be a temporary blip, the reality is that this kind of inversion has historically been a reliable predictor of recessions.

What does this mean for investors and traders? Well, it’s time to buckle up and prepare for some serious volatility in the markets.

In the past whenever we would see a yield curve inversion occur, investors would flee from stocks and into the relative safety of bonds.

But there is no indication today that bonds are safe. This is not hyperbole. The yield on the One Year T-Note is 4.42. The last Consumer Price Index report came in at 6%. The difference between the two is the real rate of return, which is currently negative.

So, any investor, trader or institution that invests in the full faith and credit of the U.S government is guaranteed a loss of 1.58%. Particularly now that the Fed has decided to backstop hundreds of billions in bank deposits it is hard to imagine a scenario where high inflation is not baked into the mix.

Now, let me break it down for you, because this debt spiral has a few key ingredients:

- Soaring borrowing costs: Picture a country neck-deep in debt. Investors get nervous and start demanding higher interest rates to offset the risk. The result? Borrowing becomes pricier for the government, adding fuel to the debt fire and pushing the fiscal situation closer to the brink.

- Crumbling fiscal position: With debt service costs skyrocketing, the government finds itself struggling to cover basic expenses or invest in essentials like infrastructure. Economic growth takes a hit, tax revenues shrink, and Uncle Sam is left scrambling to borrow even more to make ends meet.

- Vanishing investor confidence: As the debt-to-GDP ratio climbs and fiscal health deteriorates, investors become increasingly worried about the government’s ability to pay back its debts. The outcome? Capital takes flight, the currency loses value, and borrowing costs surge even higher. It’s a vicious cycle that only deepens the debt spiral.

- Stagnation or recession: The debt spiral doesn’t just hurt the government; it takes a toll on the entire economy. Slashed government spending and steep borrowing costs can grind growth to a halt or even throw the country into a recession, making it even tougher to break free from the spiral.

- Default or restructuring: If the debt spiral isn’t stopped, the government may ultimately face default or be forced to restructure its debt. That’s when the sovereign debt crisis erupts, wreaking havoc on the domestic economy and possibly even sending shockwaves through the global financial system.

All the elements are in place for this to occur. Some analysts are claiming this is what occurred in 2022 when the Fed began its interest rate increases.

So, what’s the solution? It’s simple: policymakers must put fiscal responsibility front and center, implement solid economic policies, and keep investor confidence intact. That means keeping debt levels sustainable, ensuring economic growth, and embracing transparency and good governance. By tackling the root causes of the debt spiral, governments can steer clear of a sovereign debt crisis and shield their citizens from the devastating economic fallout that often follows.

I hate to be skeptical, but this sounds like a tall order to me and unlikely to occur based on the behavior of regulators, and policymakers over the last 50 years of the great Fiat experiment. Central Banks have been calling the shots in the economy for over 110 years during which time we have seen the currency lose 98% of its purchasing power. Under the stewardship of the Fed over the last 4 decades, we have seen the financial system stumble from one crisis to the next, guaranteeing that the next crisis was an order of magnitude larger than the last one. The Fed’s response to each crisis is predictable and perverse. They expand credit, suppress interest rates, and print money. This has created perverse incentives, incredible moral hazard, and a widening wealth gap, while guaranteeing the seeds for the next crisis are planted.

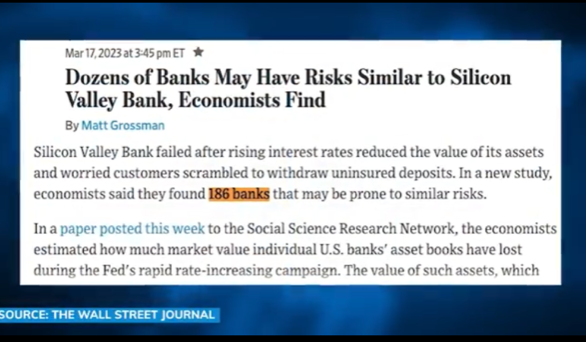

Here is what the Wall Street Journal reported three weeks ago regarding the banking crisis:

This article states that 186 banks are in a similar condition to Silicon Valley Bank!

According to the economists interviewed, many banks have engaged in similar lending practices to Silicon Valley Bank, which ultimately led to its collapse. This has raised concerns about the overall stability of the banking industry and its ability to identify and manage potential risks.

These economists urge regulators and policymakers to closely monitor the banking industry and implement measures to address potential risks.

Huh?

We have 4 major credit rating agencies in the United States and Canada who are tasked with evaluating the creditworthiness of corporations, banks, and sovereign governments.

The top four leading credit rating agencies in the world are:

Standard & Poor’s (S&P): Established in 1860, Standard & Poor’s is an American credit rating agency that provides credit ratings for sovereign governments, companies, and various financial instruments. It is a division of S&P Global and is well-known for its stock market indices, such as the S&P 500.

Moody’s Investors Service: Founded in 1909, Moody’s is another prominent American credit rating agency. It assesses the creditworthiness of governments, corporations, and various financial instruments, assigning ratings that help investors gauge the risk associated with different investments. Moody’s is a subsidiary of Moody’s Corporation.

Fitch Ratings: Fitch Ratings is the smallest of the “Big Three” credit rating agencies, with headquarters in both New York and London. Established in 1914, Fitch provides credit ratings for governments, corporations, and financial instruments, helping investors assess the credit risk associated with their investments.

DBRS Morningstar: DBRS is a Canadian credit rating agency founded in 1976, which was acquired by Morningstar Inc. in 2019. The company provides credit ratings for various entities, including governments and corporations, and covers a wide range of sectors, such as financial institutions, insurance, and structured finance.

Why is it that we have not heard a peep from these institutions over the past few weeks? Are they asleep at the wheel again? The Gold market certainly seems to think so!

I would hate to think that it is déjà vu all over again but check out the following article on Yahoo! News about Morgan Stanleys Analysts warning about serious problems in the Commercial Real Estate sector.

Lisa Shalett, the chief investment officer for Morgan Stanley Wealth Management is sounding the alarm that there are major issues in the commercial real estate sector. With the shift to remote work, vacancy rates among commercial buildings are exceeding 20%. According to Shalett, over 50% of the $2.9 trillion in commercial mortgages will need to be renegotiated in the next 24 months, with new lending rates likely to be up by 350 to 450 basis points. This is a major cause for concern, as regional banks have accounted for 70% to 80% of all new loan originations in the past cycle, and regional banks have been decimated by the recent banking crises concerns.

And the outlook for office properties isn’t looking any better. Shalett notes that vacancy rates are close to a 20-year high. Distress on this level and scale will initially hurt landlords and the bankers who lend to them but the pain will also be felt by the community itself.

When I read the article, it had all the memories and trappings of the 2008 Great Financial Crisis.

When I try to understand the problems in the economy, my conclusion is that the Fed is trapped between a rock and a hard place. If they lower rates, they are admitting defeat and accelerating the risk of inflation. If they raise rates, you will see more banking failures as bond prices will tumble. As I have written about previously, Bonds are the toxic assets of 2023. The only thing you have almost 100% certainty on is that they will always debase the currency.

What is happening in the financial markets is that traders and investors are searching for safe havens. They are not comfortable with negative real rates of returns in the bond market, but they also don’t want to expose themselves to all the volatility that is generated by interest rate increases. It’s a very challenging trading environment to say the least.

How do you go about making sense of it all? The risks are larger today than they have ever been before. That’s why trading with artificial intelligence is a necessity. Back in the 1970’s Alvin Toffler, the author of Future Shock stated that in the future, “change will happen faster and faster.” No truer words have ever been spoken.

My research is leading me to think that we are at the beginning of a commodity Supercycle boom. The primary reason for this is the persistent debasement of currency by the monetary authorities.

Watch Gold.

Watch Silver.

Watch Bitcoin.

We dig into themes like this in our Free Live Masterclass Trainings on Artificial Intelligence which I would like to invite you to attend.

What does the current financial landscape mean for you as a trader? In the last three years, we’ve witnessed a remarkable surge in money supply. As inflation rears its head, it’s clear that prices will fluctuate rapidly.

This heightened volatility presents lucrative opportunities for traders who can pinpoint the best prospects.

To thrive in these markets, you need to consistently be on the right side of the right market at the right time. Exceptional traders are fixated on minimizing losses and maintaining a disciplined approach to uncovering outstanding trade ideas, especially amidst today’s vast market distortions.

That’s why neural networks, machine learning, and artificial intelligence are indispensable for modern traders. This is the power artificial intelligence brings to the table.

The crux of successful trading lies in organizing information for effective decision-making. How have your decisions fared in the past year? How do they compare to AI-driven decisions?

While mistakes can be setbacks for humans, they pave the way to mastery and excellence for machine learning. The true value in trading comes from learning from losses and understanding why certain strategies fail. As a trader, you want to invest your hard-earned money in proven methodologies.

Humans often struggle to learn from negative experiences, as ego tends to interfere.

Since artificial intelligence has beaten humans in poker, chess, Jeopardy, and Go! why would trading be any different?

As you move forward, ponder how you’ll trade in the markets without an edge. Are you ready for the increased volatility that’s becoming the new norm?

Reflect on your past losing trades and ask yourself what you learned from those experiences. How do you analyze risk?

AI delivers knowledge—practical knowledge—and its effective application.

Artificial intelligence isn’t just a “nice-to-have” tool.

It’s an essential instrument for flourishing in today’s global markets.

We live in thrilling times.

Mistakes may be financially costly, but for machine learning, they serve as stepping stones towards mastery and excellence. The real education in trading lies in learning from losses.

Visit with us and check out the A.I. at our Next Live Training.

It’s not magic. It’s machine learning.

Make it count.

IMPORTANT NOTICE!

THERE IS SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.