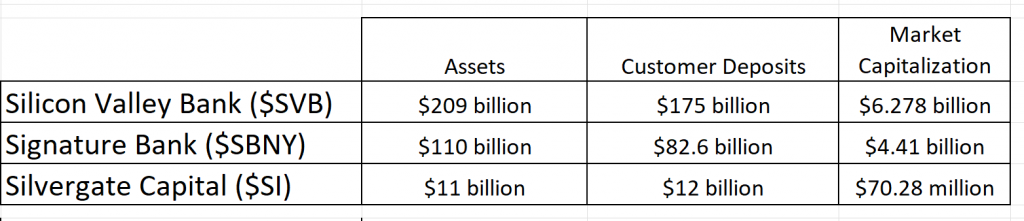

Over the past week, we have seen the failure of Silicon Valley Bank ($SIVB), Signature Bank ($SBNY) and Silvergate Bank. Yesterday, Switzerland’s Credit Suisse ($CS) added concerns to major bank contagion when it sunk to 52-week lows before receiving a bailout from the Swiss Central Bank for $57 billion. And to top it all off, the smaller banks are in a major retreat since this banking crisis began.

If we look at the chart of Credit Suisse it has been in a firm downtrend for many years. Yesterday’s price action hit a low of $1.75 which is a 95% decline from its 10 year high. Over the last 52 weeks, $CS is trading at its 7th percentile of its 52-week range. Regardless how you try to spin the price action, the entire banking sector looks ugly.

What makes this past week, so intimidating is the size of these institutions and how quickly they were shut down. Equally frustrating is the diversity of opinion surrounding the closures and what it potentially means for banking, business, and the economy as a whole.

Throughout history, banking crises have frequently surfaced, often leading to widespread economic turmoil and financial instability. At the core of these crises typically lie the complex interplay of several contributing factors. For instance, a lack of stringent regulatory oversight often paves the way for banks’ excessively risky lending practices, resulting in the build-up of precarious debt levels. Additionally, economic shocks, such as sudden changes in interest rates or currency values, can destabilize the banking sector, pushing banks towards insolvency. Misaligned incentives and moral hazard, further exacerbate the problem, as banks take undue risks in the pursuit of short-term profits. In sum, the major reasons for a banking crisis can often be attributed to insufficient regulation, economic disruptions, and the inherent nature of the banking system to engage in excessive risk-taking.

For example, the largest banking failure in the United States was Washington Mutual Bank. Washington Mutual Bank, once the largest savings and loan institution in the United States, met its demise in 2008. At the time of its failure, the institution held assets worth $307 billion, a colossal figure that marked the largest bank collapse in the country’s history. This catastrophe can primarily be attributed to the bank’s aggressive expansion strategy, which involved substantial investment in subprime mortgage loans. Regrettably, the concurrent real estate market crisis and widespread defaults on mortgage repayments wreaked havoc on the bank’s financial stability. Moreover, the management’s inability to handle risks and make prudent decisions during this critical period only exacerbated the situation, ultimately leading to the bank’s alarming collapse. The final outcome of the Washington Mutual failure is that the FDIC seized the bank and sold its assets to JPMorgan Chase for $1.9 billion.

Likewise, the failure of IndyMac in 2008 can be attributed to a combination of factors, many of which were tied to the broader financial crisis that gripped the United States during that time. As the nation faced an economic downturn, the housing market began to collapse, leading to a significant rise in mortgage defaults. IndyMac, as one of the largest savings and loans institutions in the country, specialized in high-risk mortgages known as Alt-A loans – mortgages issued to borrowers with less-than-perfect credit. These mortgages were heavily reliant on the continued appreciation of home prices, but as the housing bubble burst, IndyMac was left exposed to massive losses. Furthermore, the bank’s struggle to raise capital and maintain liquidity in the face of this crisis led to a loss of confidence and ultimately, a bank run, where panicked customers withdrew their money en masse. When IndyMac ultimately failed in July 2008, it was the second-largest bank to do so in the United States, with over $32 billion in assets held at the time. The failure rippled through the financial industry and highlighted the systemic risk presented by such risky lending practices amidst a volatile economic landscape. The outcome of the IndyMac failure is that the FDIC took over the bank and eventually sold its assets to a private equity firm.

As I try to understand the current banking crisis it appears to be much different from its predecessors. These current failed banks have failed because they were huge players in the crypto space, and simultaneously they had billions in exposure to U.S. Treasury Bonds which have retreated massively over the past year.

When banks receive deposits, traditionally they loan out a large percentage of those funds. Whatever percentage they do not loan out they are required by law to invest in the full faith and credit of the U.S government. They can invest in T-Bills, T-Notes or T-Bonds.

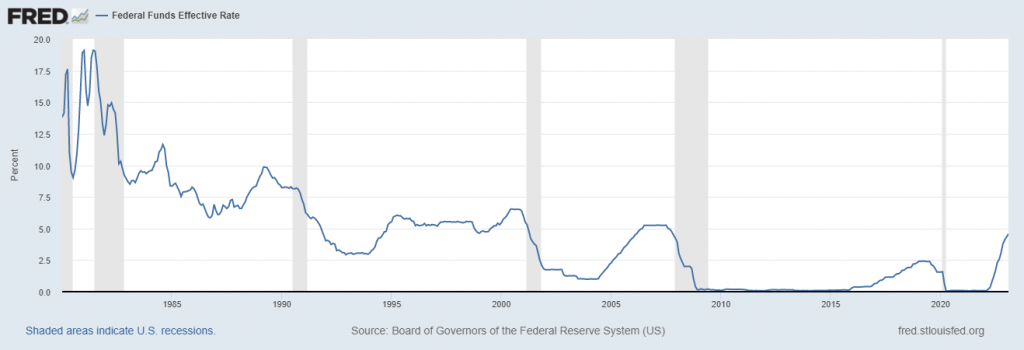

Over the last 41 years interest rates only went down in price. That all changed in 2022.

Any institution that was LONG treasuries over the last three years suffered huge price risk on their Treasury portfolio when The Fed began raising interest rates in earnest in 2022. Whenever interest rates go up, the price of fixed rate treasuries goes down. Many armchair quarterbacks are criticizing these banks for building a huge portfolio of long treasuries. I don’t understand this criticism because this is what banks always do. U.S. Treasuries are backed by the full faith and credit of the U.S. government. Criticizing a bank for owning Treasury Bonds is missing the mark. We should be demanding accountability from the Fed for manipulating the interest rate market to zero percent since the Great Financial Crisis and creating this hazard.

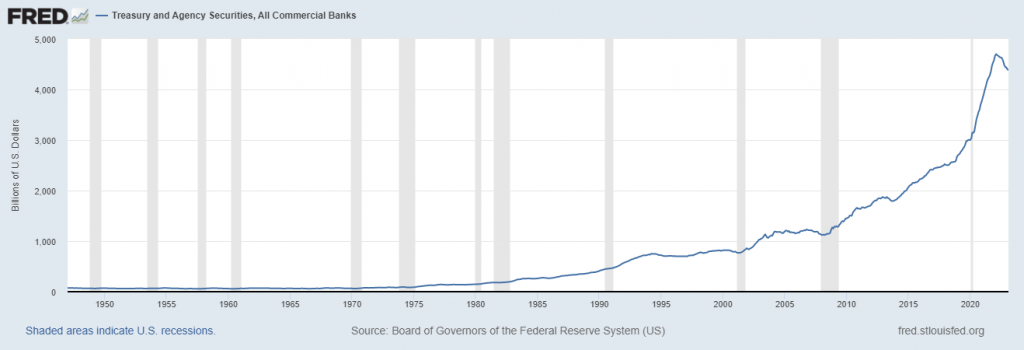

Simply look at the following chart, created by The St. Louis Fed, of the quantity of Treasury Securities held by all Commercial Banks Since the Pandemic of 2020, the quantity of Treasuries held by Commercial banks has increased by $1.5 trillion. This communicates loud and clear the level of risk that exists for any institution that was buying low yielding Treasuries in a highly inflationary environment that had the Fed raising interest rates at the fastest level in history.

Rapid interest rate increases do create a lot of risks! As a matter of fact, the estimates are that most commercial banks are carrying $600 billion in unrealized losses from their Treasury Bond portfolios. That is a massive problem because that $600 billion is the depositor’s money.

Yet, as you recall, Fed Chairman Powell’s testimony from the previous week he assured Congress that “nothing in the data suggests to me that we have tightened too much.”

But what makes this banking crisis different than previous calamities is that very few analysts want to say that this time the toxic assets are U.S. Treasury Bonds.

Stop and think about this. Whenever you take a loan from a bank, they require some form of collateral. If you borrow for a home mortgage, the home is pledged as collateral. If you buy a car, the car is pledged as collateral. If you are a manufacturing business your business machinery is pledged as collateral.

Now when a bank needs a loan from the Fed, they pledge their Treasury Bonds as collateral. Banks are in potential trouble because of the massive decline in Treasury bonds in 2022. What is noteworthy is the Feds response in these instances. They deny they created the problem and just create another ticking time bomb and try to kick the can down the road. It was the Fed that debased the value of the Treasuries.

What is most disconcerting about this attitude from the Fed is that countries who have purchased our debt for years are very aware of this. It doesn’t exactly pose confidence in the system.

Nobody wants to be politically incorrect and address the reality that even now, buying 4% government paper in a world where inflation is 6% is a toxic asset! Many banks are potentially insolvent because of this little inconvenient fact. It was the Fed that pushed interest rates to zero percent to stimulate the economy after the Great Financial Crisis and what is occurring today is directly attributed to that very poor decision.

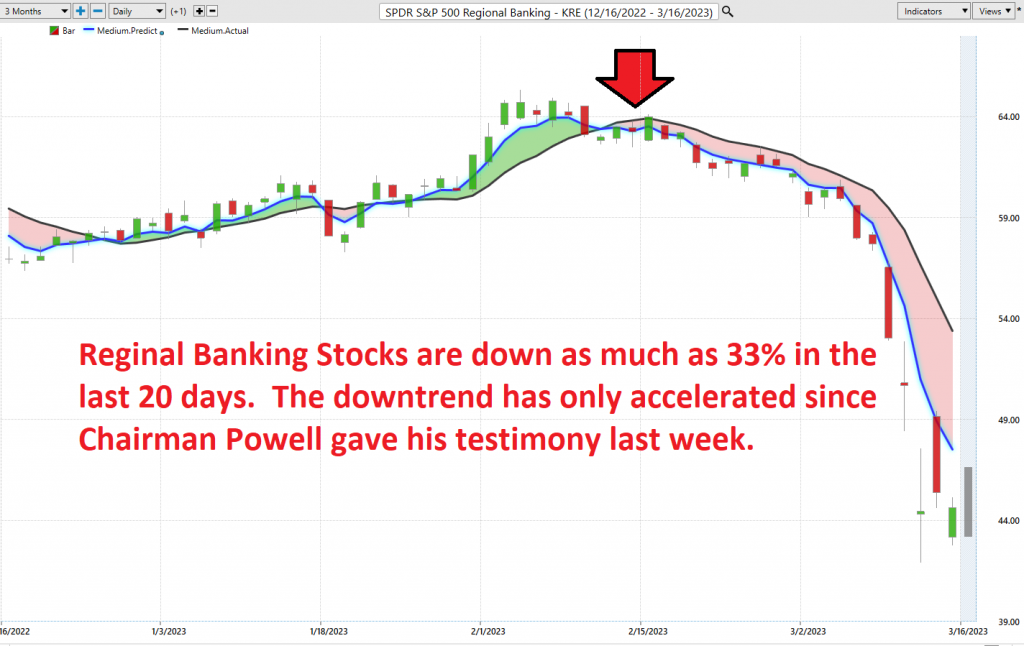

Meanwhile look at the performance of the SPDR S&P Regional Banking ETF ($KRE).

Yesterday afternoon, Barney Frank, author of the Dodd Frank Banking Reform Act, which was passed in 2010, and board member of Signature Bank gave an interview to CNBC. According to Frank:

Signature executives explored ‘all avenues’ to shore up its situation, including finding more capital and gauging interest from potential acquirers. The deposit exodus had slowed by Sunday, he said, and executives believed they had stabilized the situation.

Instead, Signature’s top managers have been summarily removed and the bank was shuttered Sunday. Regulators are now conducting a sales process for the bank, while guaranteeing that customers will have access to deposits and service will continue uninterrupted….

‘I think part of what happened was that regulators wanted to send a very strong anti-crypto message,’ Frank said. ‘We became the poster boy because there was no insolvency based on the fundamentals.’”

I find it fascinating that Mr. Frank a former politician and Board of Director of Signature Bank would be so forthright to imply that the failure of Signature Bank was essentially a “hit job.”

The more I study these banking closures the more I recognize how much risk is baked into the financial markets based upon this massive manipulation of interest rate policy. Now with $600 billion in unrealized Treasury Losses the Fed is recapitalizing banks at 100% on the dollar and we are being told this will not cause inflation.

I know how this movie ends. I’ve seen this plot many times before. It’s called currency debasement Federal Reserve style. Your money buys less and less.

How can anyone maintain confidence in the system based upon these types of financial shenanigans? How can you believe in the full faith and credit of the U.S. government when they are still offering real negative returns when adjusted for inflation?

What does this mean to you as an investor and trader?

As more and more money is being printed and the Fed continues to support financial markets it is crystal clear how fragile the economy is. In my opinion, they cannot afford to not support markets without the whole house of cards come tumbling down.

Dollars are being debased. Financial assets are increasing in price because the Fed is purchasing assets that no one else will.

While I have shared my opinion with you about what I see is the fundamental current economic environment. Artificial intelligence could not have predicted the closing of these banks. But A.I. was 100% in predicting the downtrends that all banking stocks have been on for the past 5 weeks.

My reality is always formed by what I see, hear, feel, and understand. I’ve come to appreciate that what I see, hear, feel, and understand is a very small universe indeed. Therefore, I use artificial intelligence, neural networks, and machine learning to guide my trading decisions.

Everybody has had horrible trades. The difference between the winners and losers in life is that the winners learned very powerful lessons from their losses.

Artificial intelligence is so powerful because it learns what doesn’t work, remembers it, and then focuses on other paths to find a solution. This is the Feedback Loop that is responsible for building the fortunes of every successful trader I know.

If you think about this question, you will begin to appreciate that A.I. applies mistake prevention to discover what is true and workable. Artificial Intelligence applies the mistake prevention as a continual process 24 hours a day, 365 days a year towards whatever problem it is looking to solve.

That should get you excited because it is a game-changer.

It sounds very elementary and obvious. But overlooking the obvious things often hurt a traders’ portfolio.

The basics are regularly overlooked by inexperienced traders.

It is very sad, and unnecessary in today’s day and age of machine learning and artificial intelligence.

A stock may have a very alluring story.

A stock may have a very effective management team.

A stock may have incredible earnings.

A stock may have infrastructure, partnerships, uniqueness, etc.,

But, if these elements are not reflected in the price, you are focused on what “SHOULD” occur in the market.

And the word should is responsible for more losses in trading than any other.

Bad Traders Obsess on the SHOULD. Every other word out of their mouths’ is SHOULD.

I can’t recall how many times a trader has told me all the reasons why his portfolio is heavily invested in a stock because of a great story, despite the stock being in a firm downtrend. It is horribly painful to listen to.

The beauty of neural networks, artificial intelligence and machine learning is that it is fundamentally focused on pattern recognition to determine the best move forward. When these technologies flash a change in forecast it is newsworthy. We often do not understand why something is occurring but that does not mean that we cannot take advantage of it.

I think the Fed will continue in the race to debase.

But I do not let that opinion get in the way of my trading behavior. I’ve learned to balance my analytical insight which is often wrong with the power of world class trend analysis which has proven to be up to 87.4% accurate.

Most humans have a really hard time learning from bad experiences. The ego gets in the way, every time.

Since artificial intelligence has beaten humans in Poker, Chess, Jeopardy and Go!, do you really think trading is any different?

Knowledge. Useful knowledge. And its application is what A.I. delivers.

You should find out. Join us for a FREE Live Training.

We’ll show you at least three stocks that have been identified by the A.I. that are poised for big movement… and remember, movement of any kind is an opportunity for profits!

Discover why artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

Intrigued? Visit with us and check out the a.i. at our Next Live Training.

Discover why artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

It’s not magic. It’s machine learning.

Make it count.

IMPORTANT NOTICE!

THERE IS SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.