This past week the Nobel Prize Committee in Stockholm, Sweden announced Former Federal Reserve Chairman has won the Nobel Prize in Economics. No sooner had the announcement been made that the internet was abuzz with fans and critics either praising or dismissing the announcement. It’s unquestionable Mr. Bernanke guided the Federal Reserve through the Great Financial Crisis. Fans undoubtedly see him as a heroic figure. Critics on the other hand feel Bernanke is being rewarded for creating moral hazard and simply learning how to kick the can down the road for future generations to untangle.

Ben Bernanke is an American economist who served as the Chairman of the Federal Reserve from 2006 to 2014. He is currently a Distinguished Fellow in Residence at the Brookings Institution. Prior to his role at the Fed, Bernanke was a professor at Princeton University and chaired the department of economics there. He also served as a member of the Board of Governors of the Federal Reserve System. His area of expertise is macroeconomics and monetary policy. During his time as Chairman of the Federal Reserve, Bernanke oversaw the Fed’s response to the financial crisis of 2007-2008 and the resulting “Great Recession.” This included instituting multiple rounds of so-called “quantitative easing,” or large-scale asset purchases by the Fed to inject money into the financial system and spur economic growth. Some have criticized these policies as creating moral hazard or encouraging risky behavior by making it seem like there will always be a safety net. Others have praised Bernanke for his actions, which they say prevented an even greater economic collapse. Since leaving his role at the Federal Reserve, Bernanke has been active in writing and giving speeches about his experiences during and after the financial crisis and offering consultation to hedge funds.

A favorite headline reporting Mr. Bernanke’s accolades was from the Wall Street Journal which stated: “The former Federal Reserve Chairman’s research about financial crises didn’t help prevent one in 2008.”

In his Ph.D. thesis, Ben Bernanke made a comprehensive study of the causes of the Great Depression. His research led him to conclude that the 1929 stock market crash was not the primary cause of the economic downturn. Instead, he blamed the Federal Reserve for failing to prevent the collapse of the banking system. The resulting credit crunch, he argued, was what ultimately caused the economy to contract. Bernanke’s thesis was widely acclaimed by economists and helped to solidify his reputation as one of the leading experts on the Great Depression. The research he conducted in his PhD thesis continues to be highly influential today and has shaped our understanding of how and why the economy can contract so severely.

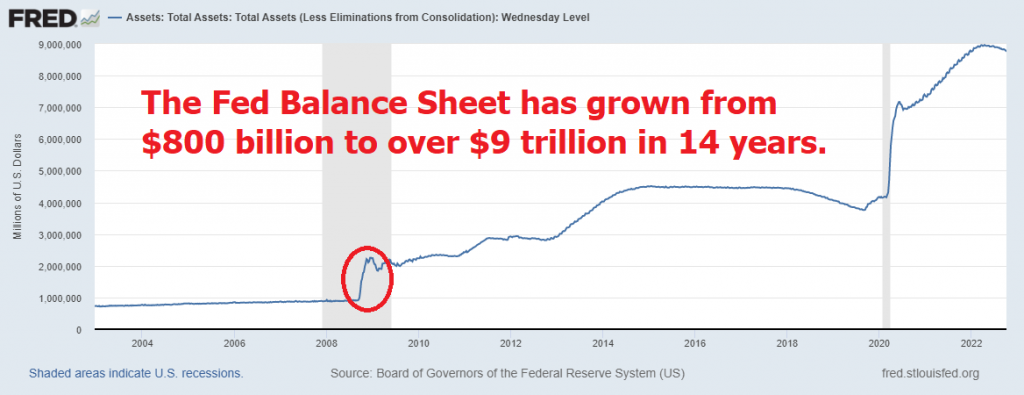

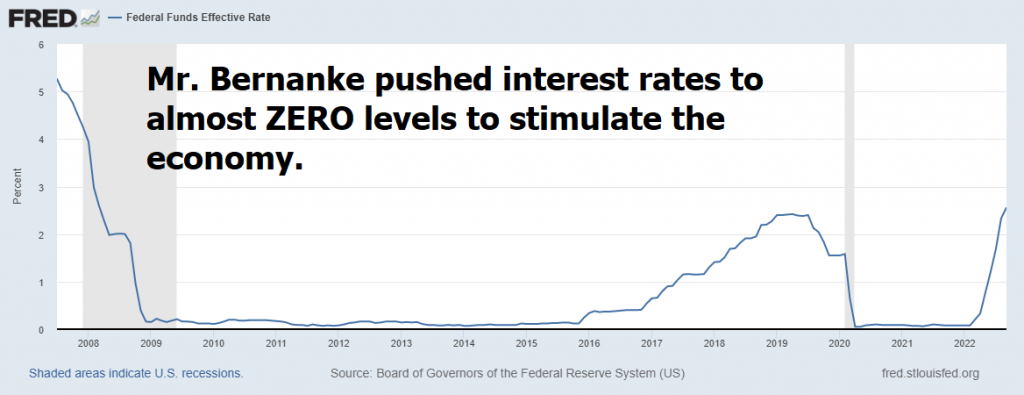

Personally, I have very mixed feeling about Bernanke receiving the Nobel Prize. True he navigated through a difficult time in the nation’s financial history, but by my interpretation, nothing has been solved. Here we are 14 years after the start of the Great Financial Crisis dealing with all of the problems that were created at Mr. Bernanke’s behest. Specifically, I am referring to the “too big to fail” policies which exponentially increased debt, fostered life support for tens of thousands of zombie companies and pushed interest rates to ZERO levels to stimulate the economy. He fostered monetary expansion which debased the currency and established the too big to fail policies which have burdened the economy with companies that could not survive without government assistance. I can only hope that future generations of monetary authorities and regulators understand the dangers associated with moral hazard which Mr. Bernanke introduced at scale to the world economy. It’s unimaginable for me to comprehend the Federal Reserve, which is the most powerful financial institution in the world, has never been audited. My suspicion is that nobody wants to know how the financial sausage is really made!

How do any of these charts above spell success for the consumer?

The most important price in a capitalist economy is the price of money. When that interest rate is pushed to ZERO percent, by monetary authorities it perpetuates moral hazard because all other price signals and relationships are distorted.

Here are my simple concerns about the Great Financial Crisis and Moral Hazard moving forward. Has anyone every been held accountable? We have had 14 years of “Too Big To Fail Policies” implemented, surely by now we can see whether or not they were productive to the economy as a whole. In Capitalism the greatest lessons are learned from failure. When businesses fail because they took dangerous risks the rest of the ecosystem learns from those experiences to make sure those actions are never perpetuated. However, if the government is going to ensure that this cannot occur, we can assume that greater reckless behavior will be engaged in moving forward with the assurance that the government will bail out the reckless decisions.

Moral hazard is a type of risk that exists when one party can make decisions that could potentially affect another party but does not have to bear the consequences of those decisions.

In the insurance industry, moral hazard can lead to increased premiums and decreased coverage for all policyholders. For example, if a driver knows that they are overly protected by liability insurance, they may be more likely to take risks on the road which could lead to an accident. In addition, if a homeowner knows that their property is over insured, they may be less likely to take measures to protect it from fire or theft. As a result, moral hazard can create an environment of unequal protection and increased costs for all involved.

The insurance industry is littered with numerous examples of moral hazard which are very easy to understand. For example, a commercial business owns a warehouse which is valued at $2 million. But it is insured at $4 million. A spectator can see how the value of this transaction creates a highly probable result where the warehouse is more valuable destroyed than functioning.

Likewise, there are several horrific incidents where organized crime has been known to rehabilitate the homeless and provide them with training to perform menial tasks. While in the process of rehabilitating them, organized crime takes out a hefty insurance policy on the formerly homeless individual. Then, months later the formerly homeless individual is found mysteriously dead creating another statistic of moral hazard.

Moral hazard is the idea that people or businesses are more likely to take risks if they believe that they will be protected from the negative consequences of those risks. There are two main types of moral hazard: moral hazard related to incentives and moral hazard related to information asymmetry. Moral hazard related to incentives occurs when people are rewarded for taking risks. For example, bankers may receive large bonuses for taking risky bets that turn out to be profitable. Moral hazard related to information asymmetry exists when one party has better information about a situation than another party.

In the context of the Great Financial Crisis, moral hazard refers to the belief that financial institutions are “too big to fail” and that they will be bailed out if they make bad decisions. This moral hazard was created by the Federal Reserve’s actions during the crisis, including its decision to bail out failing banks and its policy of keeping interest rates low. These actions made it clear to financial institutions that they would not be held accountable for their actions, and this led to a moral hazard that contributed and extended to the crisis. So much so, that we are still dealing with its aftereffects today.

Likewise, moral hazard is the idea that people or businesses behave differently when they are protected from the consequences of their actions. For example, a bank may take more risks if it knows that the government will bail it out if it gets into trouble. The argument goes that these organizations are protected from the consequences of their own bad decisions, and this gives them an unfair advantage over smaller businesses. Too big to fail also creates a moral hazard by encouraging risky behavior. If bankers know that they will be bailed out if their gamble fails, they are more likely to take risks that they would otherwise avoid. This can lead to larger financial instability and ultimately hurt the economy. Some argue that moral hazard and too big to fail are necessary evils in a capitalist system, but others believe that they are indicative of a system that is unfair and prone to cronyism.

Mr. Bernanke winning the Nobel Prize has led me to look at every decade for the last 50 years and try to better understand money in its relation to Fed policy.

The 1970’s was a period of unbridled inflation created by the War in Vietnam, the Great Society programs and funding Nasa’s space endeavors.

The 1980’s are recognized as a decade of massive dollar volatility as the world became acquainted with a pure monetary fiat system.

The 1990’s is recognized as the heyday of venture capital which transformed companies from being privately owned to publicly traded.

The 2000’s is recognized as the hangover of the 1990’s where the economy dealt with the dotcom bubble and the Great Financial Crisis.

The 2010’s is recognized as the period of great experimentation in monetary policy by the Federal Reserve amidst a backdrop of globalization.

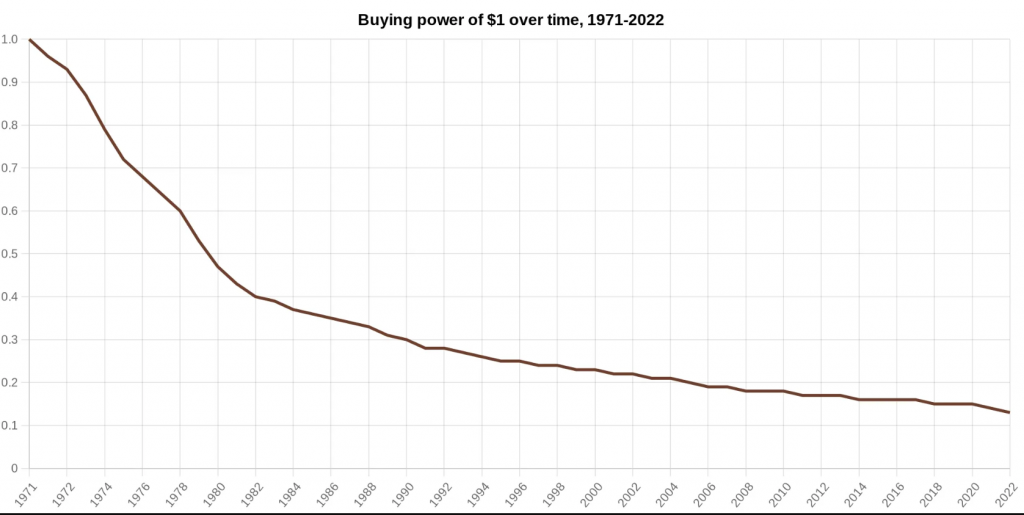

The 2020’s are shaping up to be a decade of crisis management as we continue to witness massive currency debasement due to monetary supply expansion. Look at the following chart which illustrates that in the last 51 years the U.S. dollar has lost 87% of its purchasing power.

The chart above, looked at from another perspective, is that $1 in 1971 would have to be worth $7.31 today for purchasing power to have been maintained.

The Federal Reserve System has been given a dual mandate—pursuing the economic goals of maximum employment and price stability. Does the chart above look like price stability to you?

Stability is often defined as a lack of variance or fluctuation. In other words, it is the property of a system where changes occur slowly and at a minimal level. The term can be applied to a variety of different things, including economic systems, political regimes, and even relationships. For example, an economy is said to be stable when there is little variance in prices or employment levels. A political regime is considered stable if there is minimal deviation from the status quo. And a relationship is usually considered stable when there are no major arguments or disagreements. Ultimately, the definition of stability depends on the context in which it is being used. From my perspective, when your units of purchasing power declines by 87% in 51 years that is far from stable.

But as a trader and a consumer losing on average 4% purchasing power does not fit my definition of stability which explains why I have mixed feelings about the Nobel Prize being awarded to Mr. Bernanke.

During the Great Financial Crisis, the S&P 500 was trading at 1241. Today it is trading at 3660 which represents a 195% cumulative gain. Sounds impressive until you stop and contemplate how much debt and stimulus was created to help achieve the current level. While mainstream economists would tell you there is no correlation between the two, I am not convinced.

Have you noticed that over the last year the one word you don’t hear much about any more is stimulus? And have you noticed what has happened to the stock market in its absence? Year over year the broader stock market is down over 18%

Over the past year with inflation raging as high as 9.1% traders and consumers have become obsessed with protecting their purchasing power. Rightfully so.

You may love Ben Bernanke. You might dislike him. I try not to get in debates about his policies or ideas. The bottom line is that you must protect yourself from a printing press that is the solution to every problem we face as a society.

You don’t have to win a Nobel Prize in Economics to learn how to protect your purchasing power.

Today we are riddled with unimaginable policies, debt levels and increasing interest rates. It challenges even the most sophisticated form of decision making. But it doesn’t have to be that way!

Since artificial intelligence has beaten humans in Poker, Chess, Jeopardy and Go! do you really think trading is any different?

How do you think your investment portfolio compares when pitted against artificial intelligence?

Are you capable of finding those markets with the best risk/reward ratios out of the thousands of trading opportunities that exist?

Knowledge. Useful knowledge. And its application is what A.I. delivers.

What has your performance been this year?

What’s Your Best Chance to Make Money in The Financial Markets Today?

The Answer A.I. Offers Will Surprise You. Intrigued?

You too can start finding the best trend at the right time regardless of your experience.

Intrigued? Visit with us and check out the A.I. at our Next Free Live Training.

Discover why Vantagepoint’s artificial intelligence is the solution professional traders go-to for less risk, more rewards, and guaranteed peace of mind.

It’s not magic. It’s machine learning.

Make it count.

IMPORTANT NOTICE!

THERE IS SUBSTANTIAL RISK OF LOSS ASSOCIATED WITH TRADING. ONLY RISK CAPITAL SHOULD BE USED TO TRADE. TRADING STOCKS, FUTURES, OPTIONS, FOREX, AND ETFs IS NOT SUITABLE FOR EVERYONE.

DISCLAIMER: STOCKS, FUTURES, OPTIONS, ETFs AND CURRENCY TRADING ALL HAVE LARGE POTENTIAL REWARDS, BUT THEY ALSO HAVE LARGE POTENTIAL RISK. YOU MUST BE AWARE OF THE RISKS AND BE WILLING TO ACCEPT THEM IN ORDER TO INVEST IN THESE MARKETS. DON’T TRADE WITH MONEY YOU CAN’T AFFORD TO LOSE. THIS ARTICLE AND WEBSITE IS NEITHER A SOLICITATION NOR AN OFFER TO BUY/SELL FUTURES, OPTIONS, STOCKS, OR CURRENCIES. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE DISCUSSED ON THIS ARTICLE OR WEBSITE. THE PAST PERFORMANCE OF ANY TRADING SYSTEM OR METHODOLOGY IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. CFTC RULE 4.41 – HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.